Light Commercial Vehicle Leasing Market Size

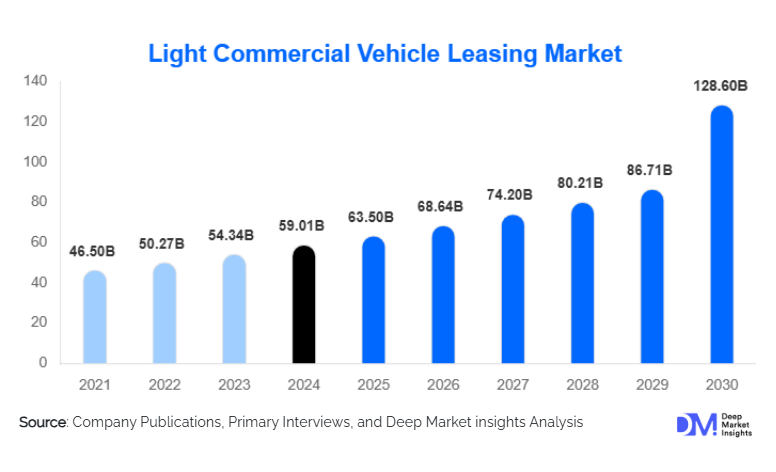

According to Deep Market Insights, the global light commercial vehicle (LCV) leasing market size was valued at USD 59.01 billion in 2025 and is projected to grow from USD 63.79 billion in 2026 to reach USD 94.16 billion by 2031, expanding at a CAGR of 8.1% during the forecast period (2026–2031). The LCV leasing market growth is primarily driven by the increasing adoption of cost-effective fleet management solutions, rapid urbanization and e-commerce growth, and rising demand for electric and technologically integrated vehicles among small and medium-sized enterprises (SMEs) and logistics operators.

Key Market Insights

- Leasing solutions are increasingly becoming a preferred alternative to vehicle ownership, enabling SMEs and large enterprises to optimize cash flow and reduce maintenance and insurance costs.

- Integration of telematics and fleet management technologies is enhancing operational efficiency, predictive maintenance, and real-time vehicle tracking, creating added value for leasing operators.

- North America dominates the LCV leasing market, with high demand from logistics, retail, and construction sectors.

- Asia-Pacific is the fastest-growing region, fueled by industrialization, urban delivery requirements, and government initiatives supporting electric mobility in countries like China and India.

- Europe shows strong demand for electric and hybrid LCVs, driven by stringent emission regulations and sustainability mandates.

- Technological adoption, including electric LCVs, telematics, and route optimization software, is reshaping operational efficiency and customer engagement.

Light Commercial Vehicle Leasing Market latest trends

Adoption of Electric and Hybrid LCVs

Leasing companies are increasingly incorporating electric and hybrid LCVs into their fleets, responding to regulatory pressures, sustainability targets, and rising environmental awareness. Governments in India, China, and Europe are offering incentives such as tax rebates, subsidies, and grants, further promoting fleet electrification. Leasing operators are collaborating with manufacturers to reduce upfront costs for customers, while expanding infrastructure such as EV charging stations, particularly in urban hubs. This trend positions LCV leasing as a crucial enabler of the low-emission logistics ecosystem.

Telematics and Smart Fleet Management

Technological integration in LCV leasing is reshaping the market. Fleet management software, GPS tracking, predictive maintenance systems, and route optimization platforms are increasingly standard offerings. These innovations reduce operational costs, enhance efficiency, and provide transparency to lessees. Businesses adopting LCV leasing with smart technologies can gain significant competitive advantages, especially in logistics, last-mile delivery, and e-commerce sectors.

Light Commercial Vehicle Leasing Market key drivers

Rising Urbanization and E-Commerce Growth

The surge in urban populations and e-commerce has significantly increased the demand for last-mile delivery solutions. LCVs, including vans and light trucks, are ideally suited for navigating congested urban areas. Leasing solutions allow businesses to quickly scale their fleets to meet fluctuating delivery demand without the burden of high capital investment.

Cost Efficiency and Operational Flexibility

Leasing LCVs provides financial and operational flexibility for businesses, particularly SMEs. Lessees benefit from predictable monthly payments, bundled maintenance, and insurance services. This reduces upfront capital expenditure and total cost of ownership, allowing enterprises to allocate resources to core business operations while accessing modern and technologically equipped vehicles.

Regulatory Compliance and Sustainability Initiatives

Governments globally are enforcing stricter emissions standards and sustainability mandates. LCV leasing operators offering electric and hybrid vehicles allow businesses to meet regulatory requirements and demonstrate environmental responsibility. Incentives such as grants, tax credits, and low-interest loans further encourage the adoption of eco-friendly fleet solutions, making LCV leasing a strategic tool for compliance.

Light Commercial Vehicle Leasing Market restraints

High Upfront Costs of Electric LCVs

Despite incentives, the high purchase price of electric LCVs remains a barrier for both leasing operators and lessees. This limits the pace of adoption and requires operators to explore cost-sharing, partnerships with manufacturers, or innovative financing solutions to make electric vehicles accessible to SMEs.

Insufficient Charging Infrastructure

The limited availability of EV charging stations in key regions, especially in developing countries, restricts the adoption of electric LCVs. Businesses may hesitate to lease electric fleets without assurance of adequate charging access, posing a critical challenge for leasing companies aiming to expand electric offerings.

Light Commercial Vehicle Leasing Market key opportunities

Government Initiatives and Policy Support

Policy-driven incentives and programs such as “Make in India” and “Made in China 2025” are boosting domestic production of LCVs and promoting fleet electrification. Leasing companies can expand their service portfolios by integrating government-supported vehicles, capturing demand from SMEs and logistics companies aiming for regulatory compliance and cost efficiency.

Expansion of E-Commerce and Last-Mile Delivery Services

The continuous growth of e-commerce has accelerated the need for last-mile delivery vehicles. Leasing operators offering flexible short- and long-term rental options can capitalize on this demand, providing scalable solutions for urban delivery fleets, seasonal peak periods, and logistics startups.

Technological Integration and Smart Mobility

Fleet management solutions, predictive maintenance, telematics, and route optimization systems are emerging as critical differentiators. Leasing companies that provide value-added services through technology can enhance customer satisfaction, reduce operational costs, and strengthen long-term contracts with enterprises.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 59.01 Billion |

| Market Size in 2026 | USD 63.79 Billion |

| Market Size in 2031 | USD 94.16 Billion |

| CAGR | 8.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Vehicle Type Insights

Vans dominate the LCV leasing market, accounting for the largest share in 2025 due to their versatility in urban deliveries and e-commerce logistics. Vans provide optimal cargo capacity, fuel efficiency, and maneuverability, making them the preferred choice for SMEs and logistics operators. Small trucks are increasingly used in construction and last-mile delivery, while pick-up trucks are gaining traction for specialized commercial applications.

Lease Type Insights

Long-term leasing is the leading segment globally, providing predictable costs, stability, and bundled services such as maintenance and insurance. This lease type is favored by logistics and service companies with consistent operational requirements. Short-term and flexible leasing solutions are also growing in popularity among startups and seasonal delivery operators.

End-Use Insights

Logistics and transportation remain the largest end-users of LCV leasing services, accounting for the majority of fleet adoption. E-commerce, retail delivery, and construction industries are the fastest-growing sectors, creating strong demand for flexible and technologically equipped vehicles. New applications, such as electric LCVs for urban micro-mobility and cold-chain delivery, are also emerging.

Explore more data points, trends and opportunities Download Free Sample Report

Light Commercial Vehicle Leasing Market Segmentations

By Vehicle Type

- Vans

- Small Trucks

- Pick-up Trucks

- Specialized Utility Vehicles

By Lease Type

- Long-Term Leasing

- Short-Term Leasing

- Flexible / Subscription Leasing

By End-User

- Logistics & Transportation

- Retail & E-Commerce

- Construction & Infrastructure

- SMEs & Service Providers

Regional Insights

North America

North America dominates the global LCV leasing market with over 30% market share in 2025. The U.S. leads due to robust e-commerce, logistics growth, and high SME adoption. Canada contributes steadily, driven by infrastructure development and urban delivery demands.

Europe

Europe holds around 28% of the market share, with Germany and the U.K. leading demand for electric and hybrid LCVs. Sustainability regulations and e-commerce expansion drive growth, while France and Italy are showing emerging interest in last-mile delivery fleets. Europe is gradually transitioning to electric LCV fleets to meet emissions targets.

Asia-Pacific

Asia-Pacific is the fastest-growing region, led by China and India, driven by rapid urbanization, industrialization, and government support for electric mobility. Logistics, SMEs, and e-commerce companies are the main adopters, with LCV leasing penetration expected to increase sharply by 2031.

Latin America

Brazil and Mexico are emerging markets with increasing adoption in retail, logistics, and infrastructure sectors. Leasing companies are gradually expanding fleets in response to industrial growth and urban delivery needs.

Middle East & Africa

The UAE and South Africa are key markets. Demand is driven by construction, logistics, and industrial sectors. Urban development and government incentives for green fleets are supporting market growth.

Key Players in the LCV Leasing Market

- Avis Budget Group

- ALD Automotive

- Arval

- Sixt Leasing

- LeasePlan Corporation

- Geotab

- Element Fleet Management

- Hitachi Capital Vehicle Solutions

- Sumitomo Mitsui Finance and Leasing

- ALD Automotive France

- Bridgestone Fleet Solutions

- Volkswagen Leasing GmbH

- Hertz Global Holdings

- EMC Leasing

- BNP Paribas Leasing Solutions