LED Neon Lights Market Size

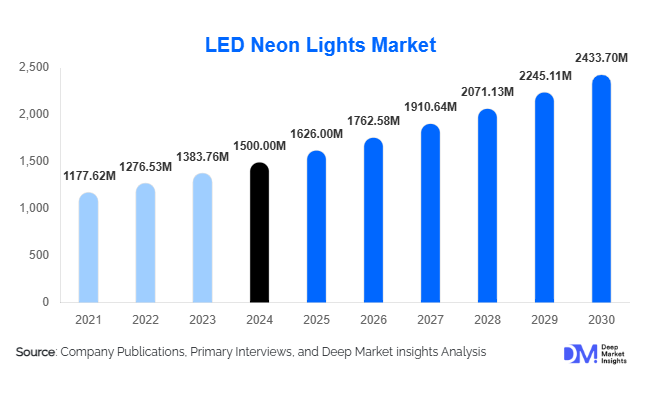

According to Deep Market Insights, the global LED neon lights market size was valued at USD 1,500 million in 2025 and is projected to grow from USD 1626.00 million in 2026 to reach USD 2,433.70 million by 2031, expanding at a CAGR of 8.4% during the forecast period (2026–2031). The LED neon lights market growth is primarily driven by the rising adoption of energy-efficient decorative lighting, growing demand for customizable signage in retail and hospitality, and the expanding use of flexible neon strips across commercial and residential applications.

Key Market Insights

- Flexible LED neon lights dominate the product segment due to their durability, versatility, and cost efficiency, capturing over 65% of the global market share in 2025.

- Architectural lighting applications account for the largest demand, representing 32% of the market in 2025, fueled by smart city initiatives and landmark illumination projects.

- Asia-Pacific leads the market, holding over 40% share in 2025, with China and India driving mass adoption through urbanization and infrastructure development.

- North America and Europe follow closely, with strong uptake in advertising signage, hospitality, and residential décor projects.

- Technology integration, including IoT-enabled smart neon systems and RGB remote-controlled strips, is emerging as a major growth enabler.

- Government energy efficiency regulations are accelerating the replacement of traditional neon with LED-based alternatives.

LED Neon Lights Market Trends

Smart and IoT-Enabled Neon Lighting

The integration of smart controls and IoT-enabled features into LED neon lighting is reshaping the market. Consumers and businesses are increasingly adopting app-controlled and voice-activated lighting systems compatible with platforms like Google Home and Alexa. This trend is particularly strong in residential and hospitality segments, where ambiance customization and energy optimization are key requirements. RGB-enabled strips with dynamic lighting modes are gaining popularity for entertainment spaces, retail branding, and architectural highlights.

Rising Demand for Sustainable and Energy-Efficient Lighting

With energy efficiency regulations tightening globally, LED neon lights are being positioned as a sustainable alternative to glass-based neon. These products consume up to 70% less electricity and last 2–3 times longer, reducing lifecycle costs for commercial and municipal projects. Growing focus on carbon footprint reduction in Europe and North America is accelerating the shift toward LED-based solutions, while APAC is adopting them to meet rapid infrastructure expansion needs.

Customization and Aesthetic Appeal

End-users increasingly demand customized shapes, colors, and lengths of LED neon lights, particularly in signage and interior décor. Manufacturers are responding with modular systems, bendable silicon tubing, and DIY-ready products. Social media-driven design trends have amplified this demand, especially in retail branding, hospitality ambience, and home improvement projects. Custom LED neon signs for events, gaming rooms, and influencer-driven setups are becoming key growth areas.

LED Neon Lights Market Drivers

Rapid Urbanization and Infrastructure Development

The global urban population expansion is fueling demand for aesthetic architectural lighting and public infrastructure illumination. Smart city initiatives in Asia-Pacific, particularly in China, India, and ASEAN countries, are deploying large-scale LED neon installations across bridges, monuments, and commercial hubs.

Increasing Demand in Retail and Hospitality

LED neon lights are widely adopted in advertising signage and branding for retail outlets, cafes, and hospitality venues. Their versatility and cost-effectiveness compared to traditional neon glass tubes make them the preferred choice for creating visually engaging spaces, directly driving sales and consumer engagement.

Energy Efficiency Regulations

Governments worldwide are phasing out inefficient lighting technologies, boosting the adoption of LED alternatives. Policies like the EU’s Energy Efficiency Directive and similar frameworks in North America and Asia are accelerating the transition to LED neon, creating long-term market stability.

LED Neon Lights Market Restraints

High Initial Setup Costs

Although cost-effective in the long run, LED neon installations can have higher upfront costs compared to traditional alternatives. For budget-sensitive end-users, particularly in developing markets, this remains a barrier to faster adoption.

Counterfeit and Low-Quality Products

The influx of low-cost imports and counterfeit LED neon products from unregulated manufacturers poses a challenge to market growth. These products often lack durability and energy efficiency, undermining consumer trust and creating price competition pressures for established players.

LED Neon Lights Market Opportunities

Integration with Smart Building Ecosystems

The rapid expansion of smart homes and connected buildings presents opportunities for LED neon light manufacturers. IoT-enabled neon systems integrated with centralized building management systems (BMS) can optimize energy consumption and enhance user control, particularly in commercial complexes and luxury residences.

Growth in Automotive Customization

LED neon lights are gaining traction in automotive applications, including interior ambient lighting and exterior customizations. With the global automotive aftermarket expected to grow steadily, neon lighting offers a lucrative niche for personalization-driven consumers, especially in North America and Europe.

Public Infrastructure and Government Projects

Government-led investments in urban beautification, public safety illumination, and tourism-focused lighting projects create significant opportunities. LED neon lights are increasingly used for bridges, highways, metro stations, and entertainment districts, particularly in the Asia-Pacific and the Middle East.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1500 Million |

| Market Size in 2026 | USD 1626.00 Million |

| Market Size in 2031 | USD 2433.70 Million |

| CAGR | 8.4% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Flexible LED neon lights continue to dominate the global market, capturing nearly 65% of the share in 2025. Their versatility, ease of installation, energy efficiency, and longer lifespan make them ideal for creative and customized designs in signage, residential interiors, architectural facades, and hospitality projects. The increasing consumer preference for personalized décor and customizable lighting solutions further reinforces demand for flexible LED neon lights. Rigid LED neon lights, while comparatively niche, are valued for their high durability and suitability for long-term outdoor installations. They are extensively used in industrial, commercial, and large-scale architectural projects where reliability and weather resistance are critical. Overall, flexible products are expected to maintain leadership due to their adaptability across both DIY and professional applications, while rigid neon lights serve as the go-to solution for heavy-duty and long-term use.

Application Insights

Architectural lighting remains the largest application segment, holding approximately 32% of the global share in 2025. This dominance is driven by rising investments in urban beautification, landmark illumination, and smart city initiatives. Large-scale projects such as commercial plazas, airports, bridges, and public spaces are increasingly adopting LED neon solutions for both aesthetic appeal and energy efficiency. Signage and advertising applications account for 28% of the market, fueled by growing demand in retail, hospitality, and entertainment sectors. Commercial adoption is being driven by businesses seeking to enhance brand visibility and customer engagement through visually striking lighting. Residential decorative applications, although smaller in overall share, are growing at the fastest CAGR of around 10.1%, thanks to increasing interest in accent lighting, modern interior décor, and customizable lighting systems that allow homeowners to personalize their living spaces. Industrial applications are witnessing steady growth as factories and warehouses adopt LED neon lights for low-maintenance, durable, and energy-efficient illumination.

Distribution Channel Insights

Offline channels currently dominate the LED neon lights market, accounting for nearly 55% of sales in 2025. Specialty lighting stores, wholesale distributors, and B2B channels remain the primary source for both commercial and industrial buyers due to personalized support, bulk ordering, and technical guidance. However, online channels are the fastest-growing segment, expected to capture over 50% of new demand by 2031. E-commerce platforms and direct-to-consumer websites are driving growth by offering global availability, customizable ordering, competitive pricing, and doorstep delivery. Increasing consumer comfort with online purchasing and the rise of digitally-savvy residential buyers are further accelerating this trend.

Explore more data points, trends and opportunities Download Free Sample Report

LED Neon Lights Market Segmentations

By Product Type

- Vegan Collagen Powders

- Vegan Collagen Capsules & Tablets

- Vegan Collagen Drinks & Shots

- Vegan Collagen Creams & Serums

- Vegan Collagen Functional Foods (Bars, Gummies)

By Application

- Nutraceuticals & Dietary Supplements

- Cosmetics & Personal Care

- Food & Beverages

- Pharmaceuticals

- Biomedical Applications

By Distribution Channel

- Online Retail (E-commerce & D2C)

- Pharmacies & Specialty Health Stores

- Supermarkets & Hypermarkets

- B2B (Clinics, Hospitals, Beauty Brands)

Regional Insights

North America

North America accounted for approximately 25% of the global LED neon lights market in 2025. The U.S. leads regional demand due to widespread adoption in retail signage, hospitality décor, commercial infrastructure, and residential projects. Drivers of growth include increasing adoption of energy-efficient and eco-friendly lighting solutions, government incentives for energy conservation, and smart city initiatives that promote modern urban illumination. Canada is witnessing steady uptake in infrastructure lighting, particularly in metropolitan projects, transportation hubs, and commercial developments. The region benefits from high disposable income, a strong preference for innovative design aesthetics, and regulatory support for energy-efficient lighting systems.

Europe

Europe holds nearly 23% of the market share in 2025, with Germany, the U.K., and France as the leading contributors. Stringent energy efficiency regulations, including the EU Energy Efficiency Directive, and financial incentives for LED adoption are major drivers of growth. Architectural, commercial, and event-based lighting applications dominate the region, while smart neon systems integrating IoT controls are gaining traction. Sustainability and eco-conscious design principles further propel the market, particularly in Western Europe, where businesses and municipalities prioritize low-energy, long-lasting lighting solutions for both indoor and outdoor projects.

Asia-Pacific

Asia-Pacific is the largest regional market, capturing over 40% of the global share in 2025. Rapid urbanization, rising disposable incomes, and expansion of retail and entertainment sectors are key growth drivers. China leads due to large-scale infrastructure projects, manufacturing capacity, and urban development initiatives. India is emerging as the fastest-growing market, fueled by residential construction, commercial developments, and affordable LED neon solutions. Japan and South Korea are mature markets, driven by advanced architectural lighting adoption and innovative interior décor applications. Government-led smart city projects, along with strong consumer interest in modern design and energy-efficient lighting, reinforce the region’s dominance.

Latin America

Latin America represents about 7% of the global LED neon lights market, with Brazil and Mexico as primary demand centers. Growth is supported by the expansion of tourism, hospitality, and commercial sectors, which are increasingly adopting decorative and signage lighting to enhance aesthetic appeal and brand presence. Regional challenges, such as higher upfront costs, are being offset by government-led incentives for energy-efficient installations and the growing awareness of low-maintenance, long-lasting lighting solutions in commercial applications.

Middle East & Africa

The Middle East and Africa collectively hold 5% of the market share in 2025. High adoption is driven by large-scale architectural projects, luxury real estate developments, and tourism-oriented urban beautification initiatives in the UAE, Saudi Arabia, and Qatar. South Africa leads adoption in the African region, particularly in commercial signage, hospitality, and entertainment venues. Government investments in public infrastructure, coupled with high disposable income in GCC countries, are facilitating LED neon light deployment for both indoor and outdoor applications.

Key Players in the LED Neon Lights Market

- Signify (Philips Lighting)

- Osram GmbH

- GE Lighting

- Acuity Brands

- NEON Flex

- Elemental LED

- Jesco Lighting

- SIDON Lighting

- Nichia Corporation

- Harvatek Corporation

- Shenzhen LEDMY Co., Ltd.

- Opple Lighting

- Zumtobel Group

- FSL Lighting

- Yaham Lighting

Recent Developments

- In June 2025, Signify launched its new line of IoT-enabled LED neon strips for smart building ecosystems, enhancing compatibility with global BMS systems.

- In April 2025, Acuity Brands expanded its decorative lighting product line with customizable LED neon strips targeting hospitality and retail customers in North America.

- In February 2025, Osram introduced sustainable silicon-based neon tubes designed to improve durability while reducing carbon emissions in production.