Jewelry Customization Service Market Size

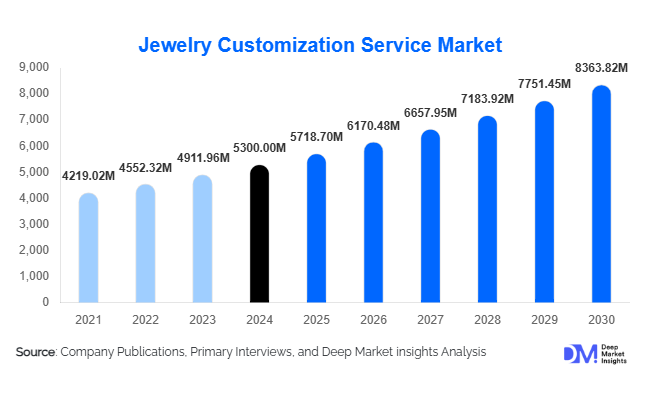

According to Deep Market Insights, the global jewelry customization service market size was valued at USD 5,300 million in 2024 and is projected to grow from USD 5,718.70 million in 2025 to reach USD 8,363.82 million by 2030, expanding at a CAGR of 7.9% during the forecast period (2025–2030). The jewelry customization service market growth is primarily driven by rising consumer demand for personalized products, technological advances in design and manufacturing, and the rapid adoption of online customization platforms across both developed and emerging markets.

Key Market Insights

- Full custom design services dominate the market, capturing more than half of global revenues in 2024 due to strong demand for engagement and heirloom jewelry.

- Rings are the most popular customized jewelry product, accounting for nearly half of the total market, driven by weddings, engagements, and gifting occasions.

- North America leads the market with around 35% share, while Asia-Pacific is the fastest-growing region, led by India and China.

- Technology adoption, including 3D CAD/CAM design, AR/VR try-ons, and AI-driven style recommendations, is enhancing consumer experience and accelerating order conversions.

- Sustainability and ethical sourcing of metals and gemstones are becoming decisive purchase factors, particularly among millennials and Gen Z buyers.

- Mid-premium customization services are expanding accessibility, appealing to middle-class consumers in both mature and emerging economies.

Latest Market Trends

Technology-Driven Personalization

Jewelry brands are integrating advanced tools such as 3D printing, CAD software, and virtual try-on applications to streamline the customization process. Consumers can co-design pieces digitally, visualize their creations before purchase, and receive faster prototyping. AI-powered recommendation engines are increasingly used to suggest gemstone cuts, metal combinations, and styles based on buyer profiles. These tools reduce uncertainty, shorten decision cycles, and improve overall satisfaction, especially among younger and digitally savvy buyers.

Sustainable and Ethical Custom Jewelry

The demand for ethically sourced materials, lab-grown diamonds, and recycled metals is reshaping the market. Consumers increasingly expect transparency around the origin of gemstones and the sustainability of metals. Jewelry customization services are responding by providing certified options, eco-friendly packaging, and recycling programs. Brands offering traceability and green credentials are capturing higher loyalty and premium pricing opportunities, particularly in North America and Europe.

Jewelry Customization Service Market Drivers

Growing Consumer Demand for Personalization

Personalization has become a defining trend in consumer products. In jewelry, customers value uniqueness, emotional significance, and identity expression. Engagement rings, anniversary gifts, and cultural jewelry are now widely personalized to reflect individual preferences. This driver accounts for the largest share of the market’s momentum in both developed and emerging economies.

Technological Innovation Enhancing Accessibility

Advancements in CAD/CAM, 3D printing, and AR/VR applications have significantly reduced customization costs and complexity. What was once an exclusive luxury service is now available at scale, empowering smaller jewelers and online brands to compete with established luxury houses. The ability to preview designs virtually and receive affordable customizations is attracting new consumer demographics.

Rise of E-Commerce and Hybrid Distribution

Online platforms are expanding market reach, enabling customers to customize and order jewelry globally. Hybrid models combining digital tools with in-store experiences are emerging, appealing to consumers who value both convenience and trust. Social media and influencer marketing have amplified awareness of custom jewelry options, accelerating adoption among millennials and Gen Z.

Market Restraints

High Costs and Lead Times

Customization inherently involves higher costs due to labor-intensive processes, premium materials, and extended design cycles. Long lead times can discourage price-sensitive or time-constrained consumers. Affordable template-based options exist, but do not fully capture the appeal of bespoke customization, limiting mass adoption.

Supply Chain Volatility

Fluctuations in the prices of gold, platinum, and gemstones, coupled with challenges in sourcing ethically certified materials, create uncertainty for both producers and consumers. Supply chain disruptions and regulatory barriers on imports and exports further constrain growth potential.

Jewelry Customization Service Market Opportunities

Integration of Emerging Technologies

Investments in AR/VR-enabled customization tools, AI design engines, and advanced 3D printing will differentiate brands and attract younger buyers. Technology-driven solutions also enable scalability, reduce errors, and enhance customer engagement, creating significant revenue potential.

Sustainability and Ethical Positioning

Brands offering certified lab-grown diamonds, recycled metals, and traceable supply chains can establish strong market leadership. Growing awareness of ethical practices is creating a profitable niche, particularly in North America and Europe, where consumers actively seek eco-friendly options.

Expansion into Emerging Markets

Asia-Pacific, the Middle East, and Latin America represent high-growth opportunities due to rising disposable incomes and cultural emphasis on jewelry. Custom bridal sets, festival jewelry, and gifting options tailored to local traditions will unlock new revenue streams in these regions.

Product Type Insights

Rings dominate the product segment, contributing about 45–50% of the market in 2024. Engagement and wedding rings lead this demand globally, driven by cultural significance and emotional value. Necklaces and bracelets are gaining traction in the fashion and gifting categories, while earrings remain a popular yet smaller segment. Brooches, pins, and cufflinks form a niche but stable market.

Service Type Insights

Full custom design services accounted for nearly 55–60% of the market share in 2024. These services deliver bespoke pieces that align with consumer preferences for exclusivity and luxury. Partial customization and engraving services are growing among budget-conscious customers, providing faster, more affordable personalization options.

Distribution Channel Insights

Online platforms captured approximately 40% of the market in 2024, reflecting growing consumer comfort with digital jewelry shopping. In-store boutiques and designer studios still retain strong importance, especially for high-value purchases, but the convenience and transparency of online configurators are fueling rapid digital adoption.

End-Use Insights

Weddings and engagements remain the leading end-use segment, representing the largest revenue driver in 2024. Fashion and lifestyle segments are rapidly expanding, particularly among younger consumers seeking everyday personalized jewelry. Gifting applications are growing steadily, supported by cultural occasions and corporate demand. Emerging niches such as wearable tech jewelry and corporate commemorative pieces are expected to add incremental growth over the next five years.

| By Product Type | By Service Type | By Distribution Channel | By End-Use |

|---|---|---|---|

|

|

|

|

Regional Insights

North America

North America held about 35% of the global market in 2024, led by the United States: high disposable income, strong online adoption, and preference for ethical customization fuel growth. Canada follows similar trends with increasing emphasis on sustainable materials.

Europe

Europe accounted for around 20% of the market in 2024. Countries such as the U.K., France, and Italy dominate demand, supported by a strong luxury heritage and preference for high-quality bespoke designs. Demand for ethically certified and eco-conscious custom jewelry is particularly high in Western Europe.

Asia-Pacific

Asia-Pacific captured nearly 30% of the market in 2024 and is the fastest-growing region, with China and India driving the bulk of demand. Rising middle-class affluence, cultural traditions around weddings and festivals, and expanding e-commerce platforms are key growth accelerators.

Latin America

Latin America accounted for 5–7% of the market in 2024. Brazil and Mexico are leading markets, driven by fashion trends and the increasing adoption of online retail. Mid-range custom jewelry appeals strongly to younger consumers in these countries.

Middle East & Africa

The Middle East & Africa represented about 7–8% of the global market in 2024, with the UAE and Saudi Arabia being dominant. Strong cultural affinity for gold and luxury jewelry, combined with rising tourism-driven purchases in Dubai, fuel market growth. South Africa also benefits from diamond-focused customization demand.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Jewelry Customization Service Market

- Tiffany & Co.

- Cartier

- Bvlgari

- Harry Winston

- Van Cleef & Arpels

- Chaumet

- Brilliant Earth

- Mejuri

- Pandora

- Gemvara

- De Beers Jewellers

- Chopard

- David Yurman

- Graff

- Swarovski (premium customized line)

Recent Developments

- In July 2025, Brilliant Earth launched a new AI-powered design platform enabling customers to co-create engagement rings online with real-time visualization.

- In June 2025, Tiffany & Co. introduced a sustainability-driven customization program offering recycled metals and lab-grown diamonds for bespoke orders.

- In April 2025, Pandora expanded its personalization services with AR-based try-on experiences across its global e-commerce platforms.