Electric Cargo Bikes Market Size

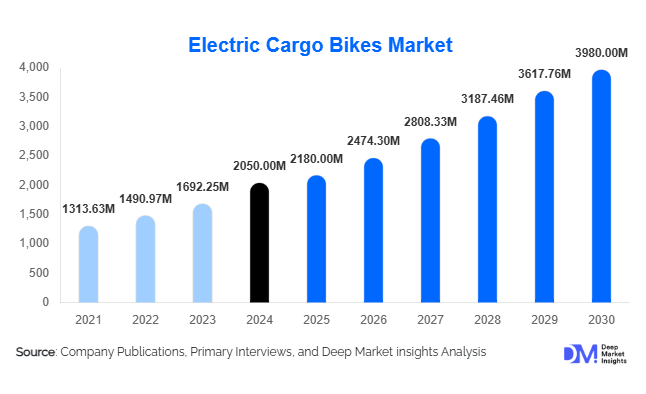

According to Deep Market Insights, the global electric cargo bikes market size was valued at USD 2,050 million in 2025 and is projected to grow from USD 2,180 million in 2026 to reach USD 3,980 million by 2031, expanding at a CAGR of 13.5% during the forecast period (2026–2031). The market growth is primarily driven by the rapid expansion of e-commerce and last-mile delivery services, increasing government incentives for sustainable urban mobility, and advancements in battery and electric drive technologies that enhance efficiency, payload capacity, and operational range.

Key Market Insights

- Urban last-mile logistics is the primary growth driver, with electric cargo bikes providing efficient, emission-free solutions for congested city environments.

- Government policies and subsidies in Europe, North America, and APAC are accelerating adoption by reducing upfront costs and supporting infrastructure development, such as dedicated bike lanes and charging stations.

- Pedal-assisted and lithium-ion battery variants dominate due to their operational efficiency, long lifecycle, and suitability for a wide range of payloads.

- Europe holds the largest share of the market, driven by countries like the Netherlands and Germany, which lead in urban delivery adoption.

- APAC is the fastest-growing region, with China and India showing rapid expansion due to urbanization, e-commerce growth, and government-backed sustainability initiatives.

- Technological integration, including IoT-enabled fleet management, GPS tracking, and smart battery monitoring, is enhancing operational efficiency and transforming logistics workflows.

Electric Cargo Bikes Market Trends

Rising Adoption of E-Commerce Logistics Solutions

Electric cargo bikes are increasingly being deployed for last-mile delivery in urban areas, particularly by e-commerce companies and courier services. Their compact size, low operating costs, and zero emissions make them a cost-effective alternative to vans for congested streets. Logistics operators are integrating electric cargo bikes into their fleets to improve delivery speed, reduce fuel expenses, and minimize carbon footprint, positioning them as a core component of sustainable urban logistics solutions.

Advancements in Battery and Electric Drive Technologies

Rapid innovation in lithium-ion and smart battery systems is expanding the range, payload capacity, and efficiency of electric cargo bikes. Features such as faster charging, energy recovery systems, and lightweight frames are becoming standard in premium models. Integration with fleet management software and IoT-enabled tracking enhances operational planning, route optimization, and predictive maintenance, providing both cost and time efficiency advantages for commercial operators.

Electric Cargo Bikes Market Drivers

Growth of E-Commerce and Last-Mile Deliveries

The surge in online retail, grocery deliveries, and urban courier services is a major driver. Electric cargo bikes provide a scalable, eco-friendly solution for navigating congested city centers, reducing reliance on conventional delivery vans. Companies are increasingly shifting to electric fleets to meet sustainability targets and reduce delivery times, particularly in Europe, North America, and APAC.

Government Incentives and Urban Policies

Regulations promoting zero-emission zones, subsidies for electric vehicle adoption, and investments in cycling infrastructure are creating a favorable environment. Countries like the Netherlands, Germany, China, and India have implemented supportive policies that encourage adoption, helping reduce operational costs and lowering the barrier to entry for fleet operators.

Technological Advancements and Operational Efficiency

Electric cargo bikes equipped with smart battery systems, GPS navigation, and IoT fleet management offer improved performance and predictive maintenance. Enhanced durability and range efficiency are making these bikes increasingly viable for commercial applications across multiple industries, from food delivery to healthcare logistics.

Electric Cargo Bikes Market Restraints

High Upfront Costs

Although operating costs are lower than conventional delivery vehicles, electric cargo bikes require significant initial investment, which can be a barrier for small businesses or independent operators. High-quality lithium-ion battery systems and durable frames contribute to the upfront cost, limiting adoption among budget-conscious segments.

Infrastructure Limitations in Emerging Markets

Limited availability of dedicated bike lanes, charging stations, and maintenance facilities in certain regions, particularly in parts of APAC, MEA, and LATAM, slows adoption. Inadequate infrastructure increases safety risks and operational inefficiencies, restricting the market's potential in these areas.

Electric Cargo Bikes Market Opportunities

Urban Logistics and Last-Mile Delivery Expansion

Growing e-commerce demand and urban congestion offer opportunities to deploy electric cargo bikes at scale. Companies can expand fleet operations, particularly in dense urban areas where conventional vehicles face restrictions. Integration with smart logistics platforms, route optimization, and fleet electrification initiatives presents avenues for profitability and market leadership.

Government Support and Incentives

Subsidies, tax breaks, and zero-emission zone regulations create opportunities for new and existing players to reduce costs and expand adoption. Governments are also investing in infrastructure improvements, such as dedicated bike lanes and public charging stations, further supporting the market’s growth potential.

Technological Innovation and Custom Solutions

New entrants and existing manufacturers can leverage advancements in battery technology, IoT-enabled fleet management, and modular cargo designs. Custom electric cargo bikes for specific industries such as healthcare, food delivery, and industrial logistics offer opportunities for differentiation, higher margins, and brand recognition. Smart features, including GPS tracking, energy-efficient motor systems, and app integration, are becoming key selling points for fleet operators.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2050 Million |

| Market Size in 2026 | USD 2180 Million |

| Market Size in 2031 | USD 3980 Million |

| CAGR | 13.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Two-wheel electric cargo bikes dominate the market, accounting for 55% of 2025 sales due to affordability, maneuverability, and suitability for congested urban areas. Three-wheel bikes provide enhanced stability and moderate payload, while four-wheel bikes cater to heavy industrial logistics. Lithium-ion battery variants are the preferred choice, holding 62% market share due to higher energy efficiency and longer lifespan. Pedal-assisted bikes, with 58% share, are favored in commercial fleets due to extended range and regulatory classification as bicycles in many regions.

Application Insights

E-commerce and retail logistics are the largest applications, representing 42% of the 2025 market share. Food and beverage delivery is rapidly growing due to online grocery and meal delivery services. Other emerging applications include healthcare logistics, pharmaceuticals, and industrial intra-logistics. Export-driven demand is particularly strong in Europe, where urban delivery fleets are increasingly adopting electric cargo bikes to comply with environmental regulations.

Distribution Channel Insights

Direct sales to fleet operators and B2B partnerships dominate the market. Online platforms and company websites are increasingly used for sales, particularly for smaller operators and urban businesses. Retail partnerships and OEM fleet deals are also common. Subscription-based fleet leasing and managed service offerings are emerging trends, particularly in Europe and North America.

Explore more data points, trends and opportunities Download Free Sample Report

Electric Cargo Bikes Market Segmentations

By Type

- Two-Wheel Electric Cargo Bikes

- Three-Wheel Electric Cargo Bikes

- Four-Wheel Electric Cargo Bikes

By Battery Type

- Lithium-Ion Batteries

- Lead-Acid Batteries

- Nickel-Metal Hydride Batteries (NiMH)

By Propulsion System

- Pedal-Assisted (Pedelec)

- Throttle-Controlled

By Load Capacity

- Up to 100 kg

- 100–200 kg

- 200–500 kg

By End-Use Industry

- E-commerce & Retail Logistics

- Food & Beverage Delivery

- Postal & Courier Services

- Industrial & Manufacturing

- Healthcare & Pharmaceutical

Regional Insights

Europe

Europe accounts for 42% of the global market, led by the Netherlands (12%) and Germany, driven by government subsidies, high e-commerce penetration, and extensive urban infrastructure. France and Italy are the fastest-growing countries due to increasing urban delivery demand and sustainability regulations.

North America

North America holds 28% of the market, with the USA leading (20%) due to robust e-commerce growth, government incentives, and adoption by large courier services. Canada follows with expanding urban logistics programs. Demand is focused on last-mile delivery solutions in congested urban areas.

Asia-Pacific

APAC is the fastest-growing region, led by China and India, driven by urbanization, e-commerce expansion, and government-backed clean mobility initiatives. Rapid adoption is expected, with high CAGR projections through 2031.

Middle East & Africa

Adoption is emerging, led by the UAE, Saudi Arabia, and South Africa. Urban delivery pilots, e-commerce expansion, and government initiatives supporting electric mobility are contributing to growth.

Latin America

Brazil, Argentina, and Mexico show gradual adoption. Export-import programs and pilot urban logistics initiatives are expanding market penetration among higher-income segments.

Key Players in the Electric Cargo Bikes Market

- Rad Power Bikes

- Yuba Electric Bikes

- Urban Arrow

- Tern Bicycles

- Riese & Müller

- Pedego Electric Bikes

- Babboe

- Carqon

- Bulls Bikes

- Xtracycle

- HNF Nicolai

- Specialized

- Kona Bikes

- Cube Bikes

- Gazelle

Recent Developments

- In March 2025, Rad Power Bikes launched a new line of modular cargo bikes with enhanced lithium-ion battery systems for extended urban range.

- In February 2025, Urban Arrow expanded operations into North American markets, targeting last-mile delivery fleets with customizable electric cargo solutions.

- In January 2025, Yuba Electric Bikes partnered with e-commerce companies in Europe to provide fully integrated delivery fleets, including smart GPS-enabled cargo tracking.