Eco-Friendly Furniture Market Size

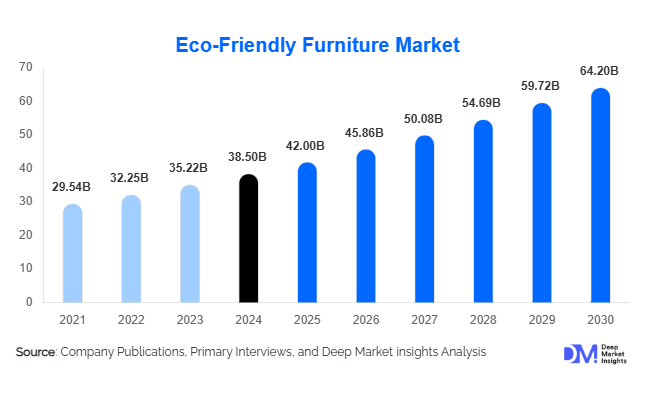

According to Deep Market Insights, the global eco-friendly furniture market size was valued at USD 38.5 billion in 2025 and is projected to grow from USD 42.0 billion in 2026 to reach USD 64.2 billion by 2031, expanding at a CAGR of 9.2% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer awareness regarding sustainability, increasing adoption of eco-friendly materials, and the expansion of green procurement practices across residential, commercial, and institutional sectors.

Key Market Insights

- Consumers are increasingly favoring eco-friendly furniture made from sustainable materials such as bamboo, recycled wood, and bioplastics, driven by environmental consciousness and aesthetic preferences.

- Online retail channels are rapidly growing, enabling direct-to-consumer access to eco-friendly furniture, especially in urban areas with high e-commerce penetration.

- North America dominates the market, supported by strict environmental regulations, high disposable income, and growing corporate sustainability initiatives.

- Europe remains a key region for growth, led by Germany, the UK, and France, where stringent eco-certification requirements and sustainability awareness are high.

- Asia-Pacific is emerging as the fastest-growing market, driven by rapid urbanization, rising middle-class income, and increasing demand in China, India, and Southeast Asia.

- Technological integration, including modular smart furniture and eco-friendly manufacturing innovations, is enhancing product functionality and consumer engagement.

Latest Market Trends

Sustainable Materials Adoption

Manufacturers are increasingly focusing on eco-certified and recycled materials to meet consumer demand for sustainable products. Bamboo, FSC-certified wood, recycled metals, and biodegradable plastics are widely adopted due to their minimal environmental impact. The trend toward modular and multifunctional furniture, combined with recycled or reclaimed materials, supports circular economy principles, appealing to environmentally conscious consumers and institutions.

Integration of Smart and Eco-Friendly Furniture

Smart furniture solutions incorporating energy-efficient lighting, IoT-enabled ergonomic monitoring, and modular design are gaining traction. These products appeal to tech-savvy consumers seeking sustainability without compromising convenience. Integration of smart functionalities into eco-friendly furniture is driving differentiation among manufacturers and creating opportunities for higher-value product lines.

Eco-Friendly Furniture Market Drivers

Increasing Environmental Awareness

Consumers and organizations are increasingly conscious of climate change, resource depletion, and waste management. The preference for furniture that reduces environmental impact has accelerated the adoption of eco-friendly alternatives in residential and commercial spaces. This trend is reinforced by social media awareness campaigns and sustainability-focused marketing strategies.

Government Policies and Incentives

Regulatory frameworks promoting sustainable manufacturing, tax benefits for eco-certification, and green procurement guidelines are encouraging manufacturers to adopt environmentally friendly practices. Incentives for using certified materials, energy-efficient production, and recycling initiatives are key drivers for market expansion.

Growth of E-Commerce Channels

Online retail has expanded the reach of eco-friendly furniture brands, offering convenience, customization options, and competitive pricing. Direct-to-consumer models allow manufacturers to engage with consumers globally, enhancing brand visibility and adoption of sustainable furniture products.

Market Restraints

Higher Cost of Sustainable Materials

Eco-friendly raw materials, certified wood, and recycled metals are costlier than conventional alternatives, limiting adoption among price-sensitive consumers. Manufacturers must balance cost efficiency with quality to remain competitive while maintaining sustainability credentials.

Limited Awareness in Emerging Economies

While urban centers are increasingly adopting eco-friendly furniture, awareness in tier-2 and tier-3 cities remains limited. This reduces market penetration in certain regions, slowing growth despite favorable long-term prospects.

Eco-Friendly Furniture Market Opportunities

Expansion in Emerging Markets

Urbanization, rising disposable incomes, and growing environmental awareness in China, India, and Brazil are creating untapped demand for sustainable furniture. Manufacturers can target underpenetrated regions with mid-range and premium eco-friendly solutions, offering growth potential for both new entrants and established players.

Smart and Sustainable Furniture Innovations

The combination of sustainable materials with smart functionalities, such as modularity, IoT integration, and ergonomic design, is a significant growth opportunity. Companies investing in technology-enabled, eco-friendly furniture can differentiate themselves in a competitive market and attract premium consumers.

Corporate and Institutional Green Procurement

Government offices, educational institutions, and hospitality sectors are increasingly adopting sustainable furniture for procurement projects aligned with ESG and green building initiatives. This segment represents high-value contracts and recurring revenue opportunities for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.5 Billion |

| Market Size in 2026 | USD 42.0 Billion |

| Market Size in 2031 | USD 64.2 Billion |

| CAGR | 9.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Indoor furniture dominates the eco-friendly furniture market with approximately 52% share in 2025. The growth in this segment is primarily driven by the rising demand for sustainable home interiors, fueled by eco-conscious homeowners seeking furniture made from certified wood, bamboo, and recycled materials. Office furniture is also experiencing notable growth as corporates adopt green building certifications such as LEED and BREEAM, prompting procurement of environmentally responsible desks, chairs, and modular workstations. Outdoor furniture is gradually gaining traction, particularly in luxury and eco-conscious landscaping projects, where consumers are increasingly designing garden and terrace spaces with sustainable, durable, and aesthetically appealing materials.

Material Type Insights

Wood-based eco-friendly furniture holds roughly 45% of the global market share in 2025, reflecting strong consumer preference for FSC-certified wood, bamboo, and reclaimed timber. The primary driver for this segment is the growing awareness of sustainable materials that combine durability, design versatility, and minimal environmental impact. Bamboo and rattan are favored for their rapid renewability, while recycled wood supports circular economy initiatives. Other materials, such as recycled metals, are increasingly adopted in commercial and industrial furniture, and bio-based plastics are gaining attention as eco-conscious alternatives to conventional plastics in furniture design.

Distribution Channel Insights

Online retail channels capture approximately 30% of the market share, with growth driven by convenience, accessibility to certified sustainable furniture, and direct-to-consumer engagement. Offline retail, including specialty stores and department stores, continues to dominate the market, with a growing focus on eco-friendly furniture sections to meet rising consumer expectations. B2B direct sales are also expanding as corporations, educational institutions, and government facilities increasingly procure large orders of green-certified furniture to comply with sustainability standards and ESG mandates.

End-Use Insights

The residential sector leads the eco-friendly furniture market with a 55% share in 2025. High demand is driven by environmentally conscious homeowners seeking sustainable décor and furniture that aligns with their values. The commercial segment, encompassing offices and hospitality, is witnessing rapid growth as companies implement green building standards and sustainability initiatives. Institutional applications, including schools, hospitals, and government facilities, are also expanding the adoption of eco-friendly furniture. Export-driven demand from North America and Europe to the Asia-Pacific further fuels market growth, particularly for high-quality, premium sustainable products.

Explore more data points, trends and opportunities Download Free Sample Report

Eco-Friendly Furniture Market Segmentations

By Product Type

- Biscuits & Cookies

- Chews & Bones

- Soft Treats

- Jerky & Meaty Snacks

- Dental Treats

- Functional/Health Treats

By Animal Type

- Dogs

- Cats

- Birds

- Small Animals

- Others (Reptiles, Exotic Pets)

By Distribution Channel

- Supermarkets & Hypermarkets

- Specialty Pet Stores

- Online Retail/E-commerce

- Veterinary Clinics & Pet Pharmacies

- Convenience Stores

By Ingredient Type

- Meat-Based

- Grain-Based

- Organic/Natural

- Functional Ingredients

By Price Segment

- Economy/Budget

- Mid-Range

- Premium

Regional Insights

North America

North America accounts for approximately 28% of the global market, led by the U.S. and Canada. The region’s growth is driven by the rising preference among millennials and Gen Z for sustainable lifestyle products, strong corporate adoption of green office initiatives, and high consumer awareness regarding environmental impact. Residential and commercial sectors are major contributors, and e-commerce platforms are facilitating wider penetration of certified eco-friendly furniture. Additionally, government policies promoting sustainability and incentives for green procurement further bolster demand.

Europe

Europe holds roughly 25% of the market, led by Germany, the UK, and France. Growth is driven by strict EU regulations on sustainability and carbon footprint, which encourage manufacturers and consumers to adopt eco-friendly furniture. High disposable incomes and increasing corporate commitments to green building certifications, such as BREEAM, further support market expansion. Eastern Europe is emerging as a high-growth sub-region, with rising awareness and adoption of sustainable materials in both residential and commercial sectors.

Asia-Pacific

Asia-Pacific is the fastest-growing region, with a projected CAGR of ~11%. Rapid urbanization, expanding middle-class populations, and increasing eco-consciousness are major drivers. China, India, Japan, and Southeast Asia are witnessing strong adoption of sustainable furniture, particularly in residential homes and mid-to-high-end commercial projects. E-commerce penetration and the availability of certified eco-friendly products are accelerating growth, while government incentives for sustainable urban development support both demand and manufacturing investments.

Latin America

Latin America, including Brazil, Argentina, and Mexico, is showing increasing demand for eco-friendly furniture, particularly among affluent consumers and environmentally aware households. Growth is fueled by rising awareness of deforestation, environmental conservation, and the need for sustainable materials. Outbound exports of eco-friendly furniture to North America and Europe complement domestic demand, while urban residential projects are incorporating sustainable furniture to meet modern design and environmental expectations.

Middle East & Africa

The Middle East & Africa, led by the UAE and South Africa, represent a growing niche market for high-end eco-friendly furniture. Regional growth is supported by significant investment in sustainable commercial infrastructure, eco-friendly hotels and restaurants, and corporate adoption of green office solutions. Rising luxury adoption and increasing sustainability awareness among institutional and residential buyers are further contributing to market expansion. Governments are promoting eco-conscious procurement, while premium residential and hospitality projects are increasingly integrating certified sustainable furniture into their designs.

Key Players in the Eco-Friendly Furniture Market

- IKEA

- Ashley Furniture Industries

- Herman Miller

- Steelcase

- La-Z-Boy

- West Elm

- Ethan Allen

- Haworth

- Knoll

- HNI Corporation

- Urban Ladder

- Godrej Interio

- NATUZZI

- Home Centre

- BoConcept