Cross-Laminated Timber (CLT) Market Size

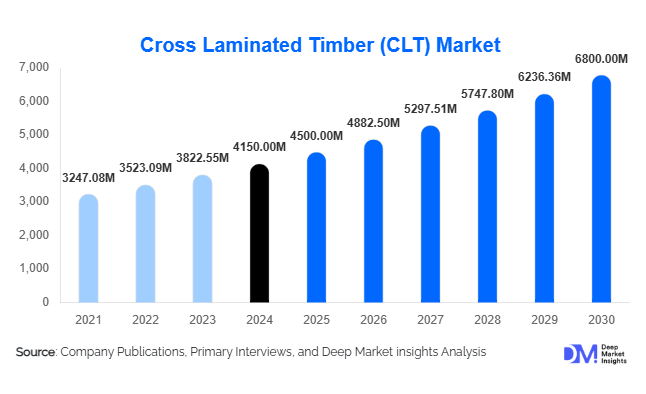

According to Deep Market Insights, the global Cross Laminated Timber (CLT) market size was valued at USD 4,150 million in 2025 and is projected to grow from USD 4,500 million in 2026 to reach USD 6,800 million by 2031, expanding at a CAGR of 8.5% during the forecast period (2026–2031). The market growth is primarily driven by rising adoption of sustainable construction materials, increased prefabricated housing projects, and government incentives promoting eco-friendly infrastructure worldwide.

Key Market Insights

- Residential and commercial construction are key adoption areas, with modular housing and office projects leveraging CLT for faster construction and sustainability.

- Technological integration in manufacturing, including automated panel production and BIM-driven design, is improving construction efficiency and panel customization.

- Europe dominates the CLT market, led by Germany and Austria, due to mature timber industries and stringent green building mandates.

- Asia-Pacific is the fastest-growing region, driven by Japan’s earthquake-resilient construction, China’s industrial growth, and India’s urban housing demand.

- North America shows strong adoption, with U.S. and Canadian construction projects emphasizing prefabrication and sustainable materials.

- Export demand is increasing, as European manufacturers supply CLT panels to APAC, LATAM, and MEA markets to meet rising construction needs.

What are the latest trends in the Cross-Laminated Timber market?

Prefabricated and Modular Construction Growth

CLT panels are increasingly used in prefabricated and modular construction, allowing off-site assembly, reduced labor costs, and faster project timelines. Urban housing projects, multi-family apartments, and commercial complexes benefit from this approach, as medium-sized panels (3–6m x 2.4m) offer an optimal balance of transportability, structural strength, and cost-efficiency. The trend is supported by growing developer preference for green and efficient construction solutions.

Fire-Resistant and Moisture-Controlled CLT Panels

To meet building codes and climate-specific demands, manufacturers are producing fire-rated and moisture-resistant CLT panels. These advancements enable broader adoption in high-rise buildings, public infrastructure, and industrial applications. Integration with BIM and advanced design tools allows precise planning of panel specifications for safety and durability, reinforcing CLT as a viable alternative to concrete and steel in environmentally sensitive projects.

What are the key drivers in the Cross Laminated Timber market?

Rising Demand for Sustainable Construction Materials

Environmental concerns and carbon emission reduction goals are driving the adoption of CLT as a renewable and low-carbon building material. Developers are leveraging CLT to achieve green certifications like LEED and BREEAM, particularly in Europe, North America, and APAC. Its renewable nature, recyclability, and lower energy footprint compared to traditional materials position it as a preferred choice in sustainable architecture.

Increased Prefabrication and Construction Efficiency

CLT’s modular and prefabricated nature reduces construction timelines and on-site labor requirements. High-rise buildings, residential complexes, and commercial offices benefit from this efficiency, driving adoption in urbanized regions. Prefabrication also minimizes material waste, lowers project costs, and aligns with sustainable construction trends globally.

Government and Private Infrastructure Investments

Public infrastructure spending and private industrial CapEx in residential, commercial, and industrial projects are positively impacting CLT demand. Initiatives such as China’s “Made in China 2025” and India’s “Make in India” indirectly support the sector by promoting modernized manufacturing and construction technologies, enabling broader CLT utilization.

What are the restraints for the global market?

High Initial Costs

The advanced manufacturing process and material sourcing of CLT make initial costs higher than conventional timber or concrete, limiting adoption among budget-sensitive developers. Small-scale residential and industrial projects often find CLT less cost-competitive.

Limited Awareness in Emerging Markets

Regions like Africa and parts of Latin America have limited knowledge of CLT benefits, coupled with scarce local production capabilities. This creates barriers to market penetration, requiring education, technical support, and investment in local manufacturing.

What are the key opportunities in the Cross Laminated Timber market?

Government Sustainability Initiatives

Governments are increasingly promoting sustainable construction through incentives, subsidies, and public procurement policies that favor eco-friendly materials. Projects like green schools, hospitals, and infrastructure developments provide substantial opportunities for CLT adoption, allowing manufacturers to secure long-term government contracts.

Technological Integration and Digital Construction

Integrating BIM, automated panel production, and prefabricated modular solutions enhances construction speed, accuracy, and scalability. Manufacturers investing in technology-driven production processes can capture larger market shares, particularly in urban centers with high construction demand.

Emerging Regional Demand

APAC and North America represent high-growth markets. Japan’s earthquake-prone areas favor CLT for lightweight structural resilience, while China and India are expanding adoption in commercial and residential construction. Export opportunities from Europe to these regions are also increasing due to quality and technological advantages.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4150 Million |

| Market Size in 2026 | USD 4500 Million |

| Market Size in 2031 | USD 6800 Million |

| CAGR | 8.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Standard CLT panels dominate globally, accounting for approximately 45% of the 2031 market share, due to their versatility and affordability. Fire-rated and moisture-resistant panels are gaining traction in high-rise and industrial projects. Acoustic panels are used in offices and hospitality projects to meet noise control requirements, while large panels (>6m x 2.4m) support industrial and infrastructure applications.

Application Insights

Residential construction remains the largest application segment (40% market share in 2031), driven by prefabricated housing and multi-family apartments. Commercial construction accounts for 35% of demand, focusing on sustainable offices, hotels, and retail spaces. Industrial buildings and public infrastructure projects are expanding in use, particularly in Europe and APAC, where government projects are incentivized to use eco-friendly materials.

Distribution Channel Insights

Direct sales to construction companies dominate CLT distribution. Online platforms and B2B marketplaces support the procurement of prefabricated panels. Export channels from Europe to APAC and North America are expanding, driven by technological superiority and established manufacturing capacity. Specialist construction consultants and architects are increasingly recommending CLT for sustainable building projects.

End-Use Insights

Residential buildings are the fastest-growing end-use segment, followed by commercial offices and public infrastructure. Multi-family apartments and government projects represent high-volume CLT demand. Export-driven growth is notable, with European manufacturers supplying APAC, LATAM, and MEA. End-use industries are expected to grow at a CAGR of 7–9% during 2026–2031, reflecting strong adoption across all sectors.

Explore more data points, trends and opportunities Download Free Sample Report

Cross Laminated Timber (CLT) Market Segmentations

By Product Type

- Standard CLT Panels

- Fire-Rated CLT Panels

- Acoustic CLT Panels

- Moisture-Resistant CLT Panels

By Application

- Residential Construction

- Commercial Construction

- Industrial Buildings

- Public Infrastructure

By Panel Size

- Small Panels (<3m x 1.2m)

- Medium Panels (3–6m x 2.4m)

- Large Panels (>6m x 2.4m)

By End-Use Industry

- Residential Buildings

- Commercial Buildings

- Public Infrastructure

- Industrial Buildings

Regional Insights

North America

North America held 28% of the global market in 2025. The U.S. and Canada are leading the demand for sustainable construction and modular housing. Developers are adopting CLT for mid-rise residential and commercial projects, leveraging prefabrication benefits and green building incentives.

Europe

Europe is the largest CLT market, accounting for 35% of global consumption in 2025. Germany and Austria are key contributors due to mature timber industries, government green building mandates, and extensive CLT expertise. Sustainable construction adoption is highest in this region, with significant exports to other regions.

Asia-Pacific

APAC is the fastest-growing region, with demand driven by Japan’s earthquake-resistant construction, China’s urban infrastructure, and India’s residential housing expansion. Increasing awareness and infrastructure development are boosting CLT adoption, particularly in commercial and public projects.

Middle East & Africa

Growth is slower due to limited local manufacturing, but mega-projects in the UAE, Saudi Arabia, and South Africa are creating niche opportunities. Adoption is primarily in commercial and high-end residential projects.

Latin America

Latin America shows moderate growth, with Brazil, Chile, and Argentina leading adoption in industrial and commercial construction. Outbound imports from Europe are gradually increasing to meet premium CLT demand.

Key Players in the Cross-Laminated Timber Market

- Stora Enso

- KLH Massivholz

- Binderholz GmbH

- Mayr-Melnhof Holz

- Structurlam

- Metsä Wood

- HASSLACHER Group

- Nordic Structures

- Schilliger Holz AG

- Schweighofer Group

- Xlam

- Massivholz GmbH

- Norbord Inc.

- Crosslam

- Smartlam