Chopping Block Market Size

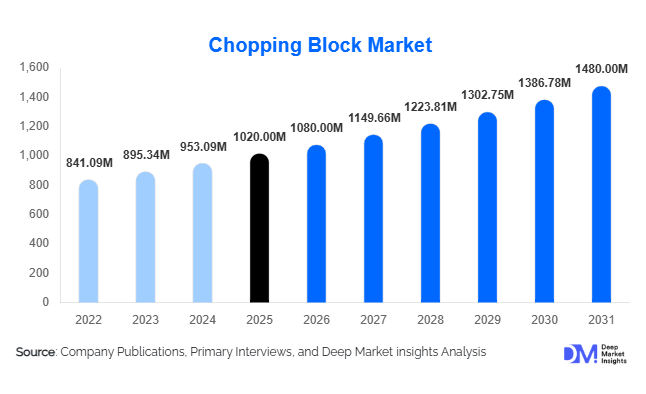

According to Deep Market Insights, the global chopping block market size was valued at USD 1,020 million in 2025 and is projected to grow from USD 1,080 million in 2026 to reach USD 1,480 million by 2031, expanding at a CAGR of 6.45% during the forecast period (2026–2031). The chopping block market growth is primarily driven by rising demand in the residential kitchen segment, recovery and expansion of the global foodservice sector, and increasing adoption of premium and sustainable materials such as hardwood, bamboo, and engineered composites.

Key Market Insights

- Premiumization of residential kitchenware is driving consumer spending on high-end end-grain butcher blocks and designer cutting boards.

- Commercial and institutional demand is increasing, with hotels, restaurants, and food processing facilities seeking durable, hygienic, and certified chopping solutions.

- North America dominates the global chopping block market, led by high consumer purchasing power and a large institutional foodservice sector.

- Asia-Pacific is the fastest-growing region, driven by urbanization, rising middle-class income, and expanding hospitality infrastructure.

- Sustainability and material innovation are reshaping the market, with composite boards, antimicrobial surfaces, and certified hardwoods gaining traction.

- Technological adoption, including CNC milling, laser engraving, and D2C e-commerce platforms, is enhancing product customization and global distribution.

Chopping Block Market latest trends

Premium and Sustainable Materials Adoption

Manufacturers are increasingly introducing end-grain hardwood butcher blocks, bamboo boards, and engineered composites to meet rising consumer preference for durable, eco-friendly, and hygienic products. The trend toward sustainable sourcing, FSC-certified wood, and antimicrobial composites is growing in both residential and commercial segments. Consumers are paying premium prices for these innovations, especially in North America and Europe, where quality and sustainability are major purchase drivers.

Digital and E-commerce Penetration

Online sales channels are driving growth in the chopping block market. Brands leverage D2C websites and marketplaces to reach global consumers with customizable, high-value products. Social media, influencer marketing, and digital customization (engraving, bundled accessories) enhance consumer engagement and facilitate premium pricing. E-commerce penetration also enables smaller artisanal brands to expand beyond local markets, capturing high-value residential and institutional buyers.

Chopping Block Market key drivers

Rising Residential and Home-Cooking Trends

Growing interest in home cooking, culinary hobbies, and social media-driven cooking content has accelerated demand for premium residential chopping blocks. Consumers are investing in large end-grain hardwood boards and butcher islands, which are valued both for functionality and kitchen aesthetics. This trend contributes to higher average selling prices and strengthens the overall market value.

Commercial Kitchen Expansion and Foodservice Recovery

Post-pandemic recovery of restaurants, hotels, and catering services has increased procurement of professional-grade chopping blocks. Institutional buyers now prefer HDPE, composite, and color-coded boards for hygiene and compliance, driving consistent B2B demand. Long-term contracts with large foodservice chains provide recurring revenue for manufacturers and help sustain market growth.

Focus on Sustainability and Hygiene

Environmental awareness and food safety regulations are encouraging the adoption of certified hardwood, bamboo, and antimicrobial composite boards. Sustainability certifications (FSC, chain-of-custody) and hygienic compliance (NSF-listed surfaces) are becoming prerequisites for both residential and commercial buyers, positively impacting premium product demand.

Chopping Block Market restraints

Regulatory Compliance and Certification Costs

Strict hygiene and food-contact regulations increase manufacturing and certification costs, particularly for smaller producers. NSF listings, European food-contact compliance, and traceability requirements create barriers for entry into institutional and export markets.

Price Competition from Low-Cost Alternatives

Plastic and mass-produced bamboo boards remain price-sensitive alternatives, especially for bulk institutional purchases. Intense price competition limits margin expansion in low- to mid-tier segments and slows penetration of premium wood and composite boards in cost-conscious regions.

Chopping Block Market key opportunities

Material Innovation and Composite Boards

Manufacturers can capitalize on the growing demand for engineered composite boards and antimicrobial surfaces that combine durability, hygiene, and knife-friendliness. Proprietary materials and high-value certifications enable premium pricing and differentiation in both residential and commercial markets.

Commercial Procurement and Foodservice Consolidation

Centralized purchasing in large restaurants, hotels, and catering chains offers opportunities for contract-based supply and bulk sales. Companies providing certified, hygienic, and scalable solutions can secure long-term, high-value B2B contracts.

Regional Growth in Asia-Pacific and Emerging Markets

Rapid urbanization, rising middle-class income, and increasing hospitality investment in Asia-Pacific, India, and Southeast Asia present growth opportunities. Local manufacturing, low-cost exports, and regional distribution networks can help new entrants capture market share in these fast-growing regions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1020 Million |

| Market Size in 2026 | USD 1080 Million |

| Market Size in 2031 | USD 1480 Million |

| CAGR | 6.45% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Wooden boards, especially hardwood end-grain butcher blocks, dominate the global market (45% share in 2025) due to premium positioning, durability, and consumer preference. Mid-market plastic and bamboo boards hold the majority of volume sales (60% value share), while composite and antimicrobial boards are emerging in commercial and high-end residential segments. Trends indicate rising adoption of custom and premium boards through e-commerce and boutique retail channels.

Application Insights

Residential kitchens lead demand (52% of market value), driven by premium home cooking and aesthetic considerations. Foodservice and institutional applications are growing rapidly, particularly in commercial kitchens, hotels, and catering services. Industrial meat processing and specialty butcher shops continue to require durable, hygienic boards. Emerging applications include cloud kitchens, retail butcher modernization, and export-driven OEM procurement.

Distribution Channel Insights

E-commerce and direct-to-consumer platforms account for 26% of global market value, enabling customization and premium pricing. Mass-market retail and specialty kitchen stores serve broader audiences, while foodservice distributors and institutional procurement channels offer high-volume, recurring sales. Online platforms and social media are increasingly influencing purchase decisions and expanding brand reach globally.

Explore more data points, trends and opportunities Download Free Sample Report

Chopping Block Market Segmentations

By Product Type

- Wooden Boards (End-Grain, Edge-Grain, Hardwood)

- Bamboo Boards

- Plastic & HDPE Boards

- Composite/Antimicrobial Boards

By Application

- Residential Kitchens

- Commercial Foodservice (Hotels, Restaurants, Catering)

- Industrial & Meat Processing

- Cloud Kitchens / Specialty Butcher Shops

By Distribution Channel

- Online Retail / D2C Platforms

- Specialty Kitchenware Stores

- Mass Retail & Department Stores

- Foodservice Distributors

- B2B Institutional Procurement

Regional Insights

North America

North America holds 38% of the 2025 market (USD 388M), driven by high consumer spending, large institutional foodservice demand, and preference for premium hardwood boards. The U.S. leads the region in both residential and commercial segments. E-commerce penetration and artisanal woodworking clusters support continued market leadership.

Europe

Europe accounts for 22% of the market (USD 224M), with strong emphasis on sustainable and certified materials. Key countries include the UK, Germany, and France. Regulatory compliance and consumer focus on hygiene and eco-friendliness shape purchasing behavior. Growth is moderate but steady, with premium segment expansion in Western Europe.

Asia-Pacific

APAC contributes 25% (USD 255M) and is the fastest-growing region. Growth is driven by urbanization, rising middle-class income, and hospitality investments in China, India, Japan, and Southeast Asia. Residential and commercial demand are both rising rapidly, with India and Southeast Asia leading volume growth.

Latin America

Latin America holds 8% (USD 82M), led by Brazil and Mexico. Demand is price-sensitive but growing due to restaurant modernization and premium urban household adoption. Customized imports and local production are emerging trends.

Middle East & Africa

The Middle East and Africa account for 7% (USD 71M), driven by luxury residential projects and hospitality infrastructure in the UAE, Saudi Arabia, and South Africa. Intra-regional travel and investment in high-end kitchens support demand growth.

Key Players in the Chopping Block Market

- John Boos & Co.

- Epicurean

- IKEA / Ingka Group

- Joseph Joseph

- Kraus

- Lipper International

- OXO / Helen of Troy

- Richlite

- SJK (European OEMs)

- Sonae (European kitchen manufacturers)

- Teakhaus

- Totally Bamboo

- Zhejiang/Guangdong cluster manufacturers

- Newell Brands (kitchenware units)

- Italian/German artisanal manufacturers