Cast Iron Cookware Market Size

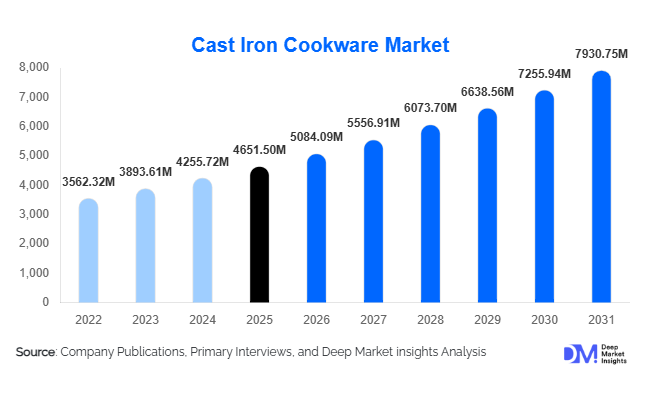

According to Deep Market Insights, the global cast iron cookware market size was valued at USD 4,651.50 million in 2025 and is projected to grow from USD 5,084.09 million in 2026 to reach USD 7,930.75 million by 2031, expanding at a CAGR of 9.30% during the forecast period (2026–2031). The market growth is primarily driven by rising health-conscious consumer behavior, premiumization of cookware, and increasing demand from both residential and commercial foodservice segments.

Key Market Insights

- Pre-seasoned and enamel-coated cookware are driving convenience-focused adoption, attracting both novice and experienced home cooks.

- Online retail channels are increasingly influencing purchasing, offering global reach, direct-to-consumer access, and customization options.

- Asia-Pacific dominates the market, particularly China and India, due to urbanization, growing middle-class households, and rising commercial foodservice demand.

- North America remains a mature and high-value market, led by the U.S. and Canada, with strong interest in premium cookware and online retail penetration.

- Europe is shifting toward premium and heritage cookware, with Germany, the UK, and France leading adoption.

- Product innovation, including lighter designs, enamel coatings, and induction compatibility, is enhancing usability and expanding market appeal.

Cast Iron Cookware Market latest trends

Premiumization and Lifestyle Positioning

Cast iron cookware is increasingly marketed as a premium lifestyle product. Luxury brands offer designer finishes, colored enamel coatings, and limited-edition collections. Consumers now view cookware as part of kitchen aesthetics, which drives demand for both functional and visually appealing cast iron products. Direct-to-consumer channels and influencer-led social media campaigns further amplify awareness of premium cookware trends. Many brands are also bundling accessories, such as seasoning kits and lid stands, enhancing the overall perceived value.

Digital & E-Commerce Influence

E-commerce platforms are reshaping cookware distribution globally. Online marketplaces allow manufacturers to reach new customers in emerging regions, provide detailed product information, and facilitate personalized recommendations. Social media engagement, digital reviews, and live cooking demonstrations are contributing to faster adoption, especially among younger demographics. Subscription and bundle-based models are emerging, allowing consumers to receive curated sets of cookware and accessories, fostering brand loyalty.

Cast Iron Cookware Market key drivers

Health & Material-Safety Awareness

Consumers are moving away from non-stick coatings and synthetic materials due to health concerns. Cast iron cookware offers chemical-free cooking, contributing to iron intake and appealing to health-conscious buyers. This trend is prevalent in both developed and emerging markets, driving widespread adoption of pre-seasoned and enamel-coated cookware.

Durability and Cooking Performance

Cast iron is valued for superior heat retention and even cooking, making it ideal for searing, frying, baking, and slow-cooking. Many households and restaurants are replacing lighter, less durable materials with cast iron due to its longevity and performance consistency. Skillets and fry pans are especially popular, leading product segments in global demand.

Growth in Home Cooking and Commercial Foodservice

Home cooking trends, fueled by lifestyle and social media, have increased demand for high-quality cookware. Simultaneously, restaurants, hotels, and catering businesses seek robust, long-lasting cookware capable of frequent use. These dual demand streams — residential and commercial — provide sustained growth opportunities for the market.

Cast Iron Cookware Market restraints

Heavy Weight and Maintenance

The intrinsic weight of cast iron and the need for regular seasoning or careful cleaning can deter first-time buyers or those seeking low-maintenance solutions. This factor limits adoption in certain demographics and residential segments.

Higher Price vs. Alternatives

Premium cast iron cookware is generally more expensive than stainless steel, aluminum, or non-stick alternatives. Price-sensitive consumers may prefer lighter or lower-cost options, which can slow growth in value-driven market segments.

Cast Iron Cookware Market key opportunities

Emerging Market Penetration and Export Potential

Emerging economies such as India and China offer high growth potential due to rising disposable incomes, urbanization, and the expansion of foodservice industries. Manufacturers in these regions also benefit from export opportunities, supplying high-demand markets like North America and Europe with premium cookware.

Channel Innovation & Digital Engagement

The rise of e-commerce, social media marketing, and direct-to-consumer strategies creates opportunities for new entrants and established players. Brands can engage younger consumers, provide customization, and offer bundled product ecosystems that increase customer loyalty and lifetime value.

Product Innovation and Premiumization

Innovation in coatings, induction compatibility, lightweight cast designs, and color options presents opportunities for differentiation. Premium and lifestyle-focused cookware allows manufacturers to capture higher margins and address consumer preferences for both function and aesthetics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4651.50 Million |

| Market Size in 2026 | USD 5084.09 Million |

| Market Size in 2031 | USD 7930.75 Million |

| CAGR | 9.30% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Pre-seasoned cast iron cookware leads the market, accounting for approximately 35% of the 2025 market (USD 1.66 billion). Ease of use, reduced maintenance, and strong performance drive its adoption. Enamel-coated variants are also growing due to aesthetic appeal and rust resistance, while unseasoned cast iron maintains niche appeal among traditional cooks.

Application Insights

Residential use dominates global demand, representing roughly 68% of the market (USD 3.24 billion in 2025). Home cooking trends, premium kitchen upgrades, and influencer-driven culinary interest fuel adoption. Commercial use in restaurants, hotels, and catering remains significant, providing stable demand and encouraging higher volume production for large-scale buyers.

Distribution Channel Insights

Online retail channels account for approximately 30% of market share (USD 1.43 billion in 2025) and are expanding fastest due to global accessibility, convenience, and targeted marketing. Supermarkets and hypermarkets retain significant volume for value and mid-range products, while specialty cookware stores support premium product sales.

Style Insights

Skillets and fry pans are the most popular style, holding approximately 42% of the 2025 market (USD 2 billion), due to their versatility across frying, searing, baking, and stovetop-to-oven cooking. Dutch ovens and bakeware are growing steadily, especially in commercial kitchens and baking-focused households.

Explore more data points, trends and opportunities Download Free Sample Report

Cast Iron Cookware Market Segmentations

By Product Type

- Pre-Seasoned Cast Iron Cookware

- Enamel-Coated Cast Iron Cookware

- Unseasoned/Traditional Cast Iron Cookware

By Application

- Residential Cooking

- Commercial Foodservice

- Baking & Roasting

- Outdoor Cooking & Camping

By Distribution Channel

- Online Retail / E-Commerce

- Specialty Cookware Stores

- Supermarkets & Hypermarkets

- Direct-to-Consumer Brand Stores

By Style / Cookware Type

- Skillets & Fry Pans

- Dutch Ovens

- Griddles & Grill Pans

- Bakeware & Roasting Pans

- Combo Cookware Sets

Regional Insights

North America

North America holds about 17% of the market (USD 809 million in 2025), led by the U.S. and Canada. Premiumization, high disposable incomes, and e-commerce penetration drive steady growth. Consumers favor high-quality, durable cookware for home kitchens and specialty cooking.

Europe

Europe represents roughly 20–25% of the market (USD 950–1,200 million). Germany, the UK, and France lead adoption with a focus on premium and heritage cookware. Sustainability, eco-friendly materials, and online availability are key growth drivers.

Asia-Pacific

Asia-Pacific is the largest region, with a 40% share (USD 1.9 billion in 2025). China and India are the fastest-growing markets due to urbanization, rising middle-class incomes, and expanding foodservice sectors. Premium and pre-seasoned cookware adoption is accelerating in both countries.

Latin America

Latin America accounts for 5–10% of the market. Brazil, Argentina, and Mexico are key countries, with growing urban middle-class households and a rise in small-scale commercial foodservice demand. Interest in outdoor cooking and premium cookware is gradually increasing.

Middle East & Africa

MEA represents 5–10% of the global market. The region benefits from tourism-driven hospitality demand, luxury hotels, and urban middle-class growth. South Africa and GCC countries (UAE, Saudi Arabia) are leading national markets.

Key Players in the Cast Iron Cookware Market

- Le Creuset

- Lodge Manufacturing Company

- Staub

- Meyer Corporation

- Tramontina

- TTK Prestige

- Vermicular

- Williams-Sonoma, Inc.

- Victoria Cookware

- FINEX Cast Iron Cookware Co.

- Camp Chef

- Calphalon

- Lava Cookware USA

- Marquette Castings

- American Metalcraft, Inc.