Camera Lens Market Size

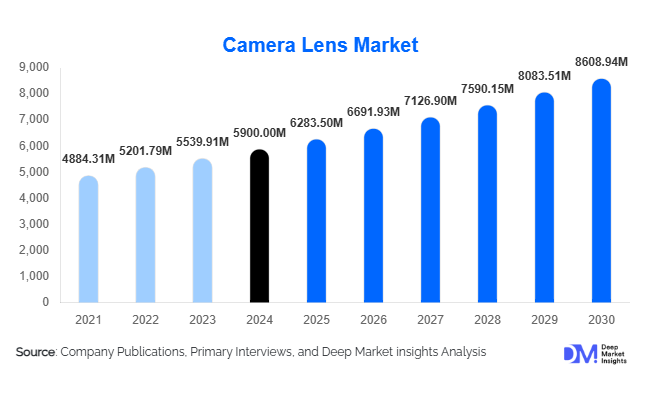

According to Deep Market Insights, the global camera lens market size was valued at USD 5,900.00 million in 2025 and is projected to grow from USD 6,283.50 million in 2026 to reach USD 8,608.94 million by 2031, expanding at a CAGR of 6.5% during the forecast period (2026–2031). The growth of the camera lens market is primarily driven by the rising adoption of mirrorless interchangeable lens systems, rapid advancements in smartphone camera modules, and increasing applications in automotive vision, surveillance, and medical imaging.

Key Market Insights

- Interchangeable lenses dominate the market, holding over 55% share in 2025, supported by the global shift from DSLR to mirrorless systems.

- Zoom lenses remain the most widely used product type, contributing nearly 35% of market revenue due to their versatility across professional and consumer applications.

- Asia-Pacific leads the global market, contributing about 40–45% of total revenues in 2025, with China, Japan, and South Korea driving both production and demand.

- Smartphone camera modules account for nearly 40% of applications, as mobile OEMs continue to integrate periscope, ultra-wide, and macro lenses into flagship devices.

- Automotive ADAS and surveillance applications are emerging as high-growth areas, boosting demand for rugged, precision-engineered optical lenses.

- The top 5 players hold about 60–65% share, though third-party brands and module specialists are increasing competition through affordable, high-quality alternatives.

Camera Lens Market Trends

Shift Toward Mirrorless Systems

The transition from DSLR to mirrorless cameras has accelerated globally, as users demand lighter systems with superior video capabilities and faster autofocus. This shift has increased sales of interchangeable lenses, particularly primes and zooms optimized for mirrorless mounts. Major players are releasing expanded line-ups of mirrorless-dedicated lenses, further solidifying this trend.

Advancements in Smartphone Lens Modules

Smartphones continue to disrupt the lens industry by integrating multiple optical modules, such as periscope telephoto, ultra-wide, and macro lenses. Demand for thin, high-quality optics has spurred R&D in folded and hybrid lenses. Computational photography paired with advanced optics is reshaping consumer imaging expectations, pushing suppliers to innovate aggressively.

Growth of Specialty Optics for Emerging Applications

Applications such as AR/VR headsets, drones, and industrial machine vision are creating new opportunities for compact, distortion-controlled optics. Similarly, automotive ADAS systems require durable wide-angle lenses for safe object detection. These emerging domains are expanding the overall demand base for camera lenses beyond traditional consumer electronics.

Camera Lens Market Drivers

Rising Popularity of Content Creation

The boom in social media, live streaming, and professional videography has spurred lens demand, as both amateurs and professionals seek specialized optics that enhance image quality. Lenses optimized for smooth video capture, wide apertures, and bokeh are increasingly in demand.

Growth in Smartphone Penetration

Smartphone OEMs continue to add multiple camera modules per device, creating a large, recurring demand for high-quality built-in lenses. Premium smartphones are integrating optical zoom and periscope modules, boosting average revenue per unit lens shipment.

Technological Innovations in Optics

Advances such as aspherical elements, advanced coatings, and hybrid materials are enabling lenses that are lighter, sharper, and more durable. These innovations not only attract professionals but also reduce costs for mass-market segments.

Camera Lens Market Restraints

Smartphone Substitution Effect

As smartphone cameras improve with computational photography, many casual consumers are opting out of purchasing standalone cameras and lenses. This cannibalizes entry-level lens demand, especially compact and budget lenses.

High Manufacturing Costs

Premium lens production involves costly raw materials, precision optics, and coatings. Combined with supply chain risks for optical glass and rare earth elements, these costs limit adoption in mid and low-tier segments and squeeze profit margins.

Camera Lens Market Opportunities

Automotive Vision and ADAS Integration

The rise of autonomous driving and advanced driver-assistance systems is generating strong demand for wide-angle and high-precision lenses. Opportunities exist for ruggedized optics capable of handling extreme environmental conditions while delivering distortion-free imaging.

Expansion into AR/VR and Industrial Imaging

The growing adoption of AR/VR devices, drones, and machine vision systems requires compact, specialized optics. Manufacturers who innovate in this space can capture early-mover advantage in high-growth, non-traditional markets.

Geographic Expansion into Emerging Markets

Rising disposable incomes in India, Southeast Asia, and Latin America present opportunities for lens makers to capture demand from first-time buyers of professional-grade cameras and smartphone modules. Government initiatives such as "Make in India" are also encouraging localized lens production.

Product Type Insights

Zoom lenses account for the largest share at around 35% of revenues in 2025, favored for their versatility across focal lengths. Prime lenses remain popular in professional and artistic photography due to sharpness and wide apertures, while specialty optics like fisheye and macro are carving out fast-growing niche demand. Telephoto lenses dominate wildlife and sports photography, representing a high-value but lower-volume segment.

Application Insights

Product Type Insights

Zoom lenses account for the largest share at around 35% of revenues in 2025, favored for their versatility across focal lengths. Prime lenses remain popular in professional and artistic photography due to sharpness and wide apertures, while specialty optics like fisheye and macro are carving out fast-growing niche demand. Telephoto lenses dominate wildlife and sports photography, representing a high-value but lower-volume segment.

Application Insights

Smartphone camera modules dominate demand with nearly 40% share in 2025, thanks to multi-camera designs in high-end devices. Professional photography and videography remain robust, supported by demand for mirrorless systems. Surveillance and automotive applications are among the fastest-growing segments, driven by security projects and ADAS adoption. Medical imaging and machine vision are smaller but expanding high-margin applications.

| By Product Type | By Application | By Distribution Channel |

|---|---|---|

|

|

|

Regional Insights

North America

North America contributes about 25–30% of the global market, led by the U.S., with strong demand for professional photography, videography, and automotive applications. Canada shows steady growth in surveillance and consumer imaging adoption.

Europe

Europe represents around 15–20% of the market, with Germany, the U.K., and France driving demand for premium optics and industrial imaging. The region’s legacy optics manufacturers continue to support specialized niches such as scientific and cinematic lenses.

Asia-Pacific

Asia-Pacific dominates the global market with a 40–45% share in 2025, supported by strong production bases in China, Japan, South Korea, and Taiwan. Rising middle-class demand in India is further accelerating regional growth. Asia-Pacific is also the fastest-growing region, with China and India expected to show the highest CAGR through 2031.

Latin America

Latin America contributes a modest but rising share, led by Brazil and Mexico. Growth is supported by increasing smartphone penetration and rising interest in professional and surveillance optics.

Middle East & Africa

MEA markets remain small but are expanding, driven by government-led smart city initiatives and infrastructure security programs. The UAE and Saudi Arabia are leading importers of high-performance surveillance and automotive lenses.

| North America | Europe | APAC | Middle East and Africa | LATAM |

|---|---|---|---|---|

|

|

|

|

|

Key Players in the Camera Lens Market

- Canon Inc.

- Sony Corporation

- Nikon Corporation

- Fujifilm Holdings Corporation

- Panasonic Holdings Corporation

- Sigma Corporation

- Tamron Co., Ltd.

- Carl Zeiss AG

- Leica Camera AG

- OM Digital Solutions (Olympus)

- Samyang Optics

- Largan Precision Co., Ltd.

- Sunny Optical Technology Group

- Genius Electronic Optical

- Sekonix Co., Ltd.