Anime Merchandising Market Size

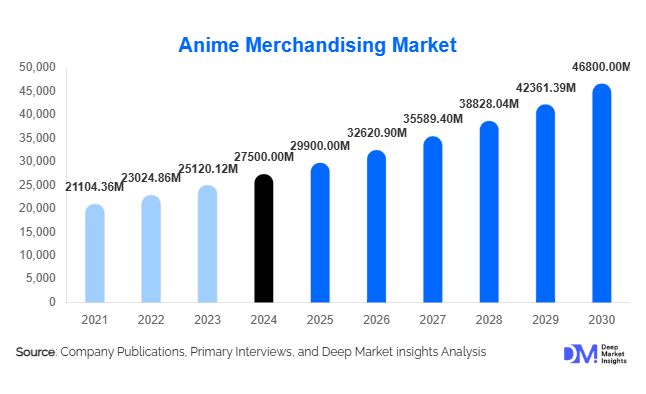

According to Deep Market Insights, the global anime merchandising market size was valued at USD 27,500 million in 2025 and is projected to grow from USD 29,900 million in 2026 to reach USD 46,800 million by 2031, expanding at a CAGR of 9.1% during the forecast period (2026–2031). The growth of the anime merchandising market is primarily driven by the increasing global popularity of anime culture, rising adoption of collectibles and apparel, and expansion of digital merchandise such as NFTs and in-game products targeting tech-savvy fans worldwide.

Key Market Insights

- Anime merchandising is experiencing strong adoption across digital and physical channels, reflecting fan engagement through collectibles, apparel, and digital goods.

- Figurines and collectibles dominate the market, fueled by limited-edition releases and a global culture of high-value fan collectibles.

- North America holds a significant market share, led by the U.S. and Canada, driven by high disposable income and e-commerce penetration.

- Asia-Pacific is the fastest-growing region, supported by Japan’s established production ecosystem and emerging markets like India and Southeast Asia.

- Europe is witnessing robust growth, particularly in Germany, the U.K., and France, with licensing partnerships and fan conventions fueling demand.

- Technological integration, including AR/VR collectibles, blockchain-based merchandise, and interactive fan experiences, is reshaping engagement and driving higher revenues.

Latest Market Trends

Rise of Collectibles and Limited-Edition Merchandise

The market is increasingly dominated by high-value figurines, action figures, and limited-edition collectibles. Fans are willing to pay premium prices for authenticity and exclusivity, which has led to a thriving secondary market. Popular franchises such as Dragon Ball, Naruto, and One Piece consistently release special editions that sell out rapidly. Collectible culture is further supported by fan communities, social media, and auction-based online platforms, allowing companies to create hype and generate higher margins.

Digital Merchandise and NFTs

Digital collectibles, including NFTs and in-game merchandise, are becoming mainstream among anime fans. Companies are exploring blockchain-powered collectibles and virtual avatars, creating unique fan experiences while monetizing digital engagement. AR/VR integration allows fans to interact with characters virtually, expanding revenue beyond traditional physical merchandise. This trend is particularly popular among Gen Z and millennial consumers, driving higher adoption of limited-edition and premium digital assets.

Anime Merchandising Market Drivers

Global Popularity of Anime Culture

Anime has evolved into a global cultural phenomenon, with streaming platforms making content widely accessible. This has expanded fan bases in North America, Europe, and APAC, fueling demand for merchandise including apparel, figures, and collectibles. Increased fan engagement through social media, conventions, and online communities amplifies merchandise consumption and repeat purchasing behavior.

Growth of E-Commerce Channels

Online retailing provides fans worldwide with easy access to anime merchandise. E-commerce accounts for nearly 48% of market revenue in 2025, supported by platforms offering pre-orders, international shipping, and exclusive releases. Digital marketing, social media integration, and influencer collaborations further enhance fan engagement, making online channels a key driver of growth.

Limited-Edition and Collector Culture

The popularity of limited-edition figures, apparel, and collectibles encourages premium pricing and repeat purchases. Collectors actively seek authenticity and exclusivity, contributing to higher margins and market stability. This trend drives both domestic and international demand, particularly in Japan, the U.S., and Germany.

Market Restraints

High Licensing Costs

Official licensing fees for popular anime franchises can be significant, limiting participation by smaller companies and raising product prices. This can constrain growth in certain segments and restrict market entry for emerging players, particularly in developing regions.

Counterfeit Merchandise

The proliferation of unlicensed and counterfeit merchandise, especially in APAC and LATAM, reduces brand value for official merchandise providers. It creates price competition and hinders revenue growth for licensed product manufacturers, challenging the market’s long-term profitability.

Anime Merchandising Market Opportunities

Expansion into Emerging Markets

Southeast Asia, Latin America, and the Middle East are experiencing rising anime fandom, driven by streaming platforms and social media. Localized merchandise, regional influencer collaborations, and partnerships with local distributors can help companies tap into these emerging markets. This opportunity allows new entrants and existing players to diversify revenue streams and gain an early-mover advantage.

Digital & Interactive Merchandise

Investment in AR/VR collectibles, NFTs, and in-game merchandise presents a high-growth opportunity. Fans are increasingly interested in digital collectibles, creating recurring revenue streams. Companies offering blockchain authentication, virtual avatar interactions, and gamified fan engagement can enhance brand loyalty and command premium pricing.

Strategic Licensing & Collaborations

Licensing partnerships with popular anime studios and global brands unlock new product lines and wider consumer reach. Collaborations with fashion brands, lifestyle products, or gaming franchises allow companies to create limited-edition, co-branded merchandise, driving exclusivity and higher fan engagement.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 27500 Million |

| Market Size in 2026 | USD 29900 Million |

| Market Size in 2031 | USD 46800 Million |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Figurines and collectibles dominate the market, accounting for 38% of the total market share in 2025. High-quality action figures, PVC models, and plush collectibles are highly sought after, with limited editions fueling secondary market activity. Apparel and lifestyle merchandise also contribute significantly, driven by cosplay trends and branded fashion collaborations. Digital merchandise, though smaller in volume, is growing rapidly due to the popularity of NFTs and virtual collectibles.

Distribution Channel Insights

Online retail dominates with 48% of market share in 2025, providing global reach and convenience for fans. E-commerce platforms facilitate pre-orders, exclusive product launches, and international shipping. Offline retail, including specialty stores and conventions, remains important for collector engagement and impulse purchases. Emerging channels include subscription boxes and fan club memberships offering exclusive merchandise.

End-Use Insights

Consumers/collectors represent the largest end-use segment, driving demand for high-value figurines, apparel, and collectibles. Gaming and digital communities are increasingly adopting digital merchandise and NFTs, while retail and entertainment outlets contribute to secondary sales. Export-driven demand from Japan, the U.S., and Europe constitutes over 30% of total market revenue in 2025. Emerging applications include gamified merchandise, subscription boxes, and fan-driven digital collectibles.

Explore more data points, trends and opportunities Download Free Sample Report

Anime Merchandising Market Segmentations

By Product Type

- Figurines & Collectibles

- Apparel & Clothing

- Stationery & School Supplies

- Home Decor & Lifestyle Products

- Digital Merchandise (NFTs, Virtual Avatars, In-Game Items)

By Merchandise Type

- Licensed Merchandise

- Unlicensed Merchandise

By Distribution Channel

- Online Retail (E-commerce Platforms, Official Stores, Fan Marketplaces)

- Offline Retail (Specialty Stores, Comic Shops, Pop-Up Stores, Department Stores)

Regional Insights

North America

North America holds 28% of the global market in 2025, led by the U.S. and Canada. High disposable income, strong e-commerce infrastructure, and a culture of collectibles drive demand. Exclusive releases and event-based merchandise contribute to robust sales growth.

Europe

Europe accounts for 22% of the market, with Germany, the U.K., and France leading. Licensing collaborations, conventions, and fan communities contribute to rapid growth. Younger consumers are increasingly embracing both collectibles and digital merchandise.

Asia-Pacific

APAC represents 42% of the global market, dominated by Japan and South Korea. Japan is a production hub and exporter, while Southeast Asia is the fastest-growing sub-region. Rising middle-class populations and increasing online access drive merchandise adoption.

Latin America

Brazil and Mexico are key markets in LATAM, though the overall share is 8%. Outbound purchases and fan conventions are emerging as growth drivers, particularly among younger demographics.

Middle East & Africa

UAE, Saudi Arabia, and South Africa are leading MEA markets. Growing disposable incomes, online adoption, and fan culture drive demand for anime merchandise. Intra-African demand is also rising, fueled by regional conventions and online communities.

Key Players in the Anime Merchandising Market

- Bandai Namco Holdings

- Good Smile Company

- Funimation (Sony)

- Aniplex

- Kotobukiya

- Banpresto

- Medicom Toy

- Sega Toys

- Square Enix

- Taito Corporation

- Megahouse

- Alter Co., Ltd.

- Hobby Japan

- Animate

- Tokyo Otaku Mode