Air Quality Monitoring System Market Size

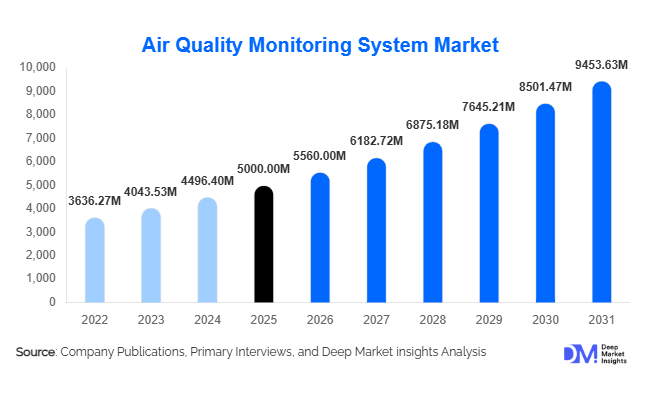

According to Deep Market Insights, the global Air Quality Monitoring System market size was valued at USD 5,000 million in 2025 and is projected to grow from USD 5,560 million in 2026 to reach USD 9,453.63 million by 2031, expanding at a CAGR of 11.2% during the forecast period (2026–2031). The market growth is driven by increasing urban air pollution, stringent government regulations, rising health awareness, and the adoption of advanced IoT- and AI-enabled monitoring technologies that provide real-time, actionable air quality data.

Key Market Insights

- Outdoor air quality monitoring systems dominate the market, addressing high pollution levels in urban and industrial areas and forming the backbone of regulatory compliance networks worldwide.

- Integration of IoT and AI into monitoring systems is enhancing predictive analytics, automated reporting, and real-time alerts, improving efficiency for both governmental and industrial stakeholders.

- North America holds the largest market share, with the U.S. and Canada leading adoption due to stringent environmental regulations and well-established air quality monitoring infrastructure.

- Asia-Pacific is the fastest-growing region, fueled by rapid urbanization, industrialization, and government initiatives in countries like China and India to combat increasing air pollution levels.

- Europe maintains steady growth due to high environmental awareness, robust legislative frameworks, and continuous upgrades of monitoring infrastructure.

- Public awareness and health concerns are driving the adoption of both indoor and outdoor air quality monitoring solutions in residential, healthcare, and educational settings.

What are the latest trends in the air quality monitoring system market?

Smart and Connected Monitoring Solutions

Air quality monitoring systems are increasingly leveraging IoT connectivity, cloud computing, and AI-driven analytics to provide real-time air quality insights. Smart sensors now transmit data to centralized platforms for predictive modeling, alert generation, and compliance reporting. These trends enable governments, industrial units, and smart cities to respond proactively to pollution spikes. Additionally, portable and wearable AQMS devices are emerging to monitor individual exposure in real-time, catering to personal health awareness.

Adoption of Low-Cost Sensors for Widespread Deployment

Technological advancements have lowered the cost of air quality sensors, enabling broader deployment in residential areas, schools, and small-scale industries. These cost-effective sensors complement high-end continuous monitoring systems, providing dense monitoring networks and granular data to inform public policy and community initiatives. Crowdsourced data collection is also gaining momentum, enhancing public engagement and localized pollution mapping.

What are the key drivers in the air quality monitoring system market?

Stringent Environmental Regulations

Governments worldwide are implementing stricter air quality standards, compelling industrial, commercial, and municipal entities to invest in air quality monitoring systems. Compliance with laws such as the Clean Air Act in the U.S., the National Clean Air Programme in India, and the EU Ambient Air Quality Directives is driving consistent demand across regions.

Urbanization and Industrialization

Rapid urbanization and expanding industrial operations contribute to higher emissions of pollutants like NO₂, SO₂, and particulate matter. The need to monitor these emissions for public health and environmental sustainability is creating sustained demand for both fixed and portable AQMS solutions. Urban centers are deploying smart city networks integrated with air quality monitoring, further boosting adoption.

Technological Advancements

AI, IoT, cloud analytics, and advanced sensor technologies are improving the data precision, reliability, and predictive capabilities of monitoring systems. Real-time alerts, automated reporting, and cloud-based dashboards are now standard features, enabling better regulatory compliance, health risk management, and industrial safety oversight.

What are the restraints for the global market?

High Initial Investment

Deploying comprehensive AQMS infrastructure, particularly continuous outdoor monitoring networks, requires significant capital expenditure, including sensor hardware, installation, and maintenance. This is a key restraint, especially in developing economies with limited public funding for environmental monitoring projects.

Data Privacy and Security Concerns

The collection, storage, and transmission of air quality data, especially from residential and indoor sensors, raise privacy concerns. Unauthorized access or misuse of location-linked pollution data could slow down adoption and necessitate robust cybersecurity measures, adding to operational costs.

What are the key opportunities in the air quality monitoring system market?

Government-Led Environmental Initiatives

Governments are increasingly funding large-scale air quality monitoring projects to meet climate goals and public health targets. Programs like China’s “Air Pollution Prevention Action Plan” and India’s “National Clean Air Programme” create opportunities for both local and global AQMS providers. Funding and incentives are expected to increase system deployments in urban and industrial zones.

Integration with Smart Cities and IoT

Urban centers are adopting smart city frameworks that integrate air quality monitoring with traffic management, energy consumption, and public health systems. AQMS providers have the opportunity to deliver connected solutions, including IoT-enabled sensors, predictive analytics platforms, and automated reporting tools for municipal and industrial applications.

Rising Public Awareness and Healthcare Applications

Increasing awareness of the health impacts of poor air quality is driving demand for indoor and wearable monitoring solutions in residential, healthcare, and educational environments. Opportunities exist for developing AI-driven predictive models, portable personal monitors, and cloud-based dashboards tailored to health-conscious consumers and organizations seeking to reduce exposure risks.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 5000 Million |

| Market Size in 2026 | USD 5560 Million |

| Market Size in 2031 | USD 9453.63 Million |

| CAGR | 11.2% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Outdoor air quality monitoring systems dominate the market, accounting for approximately 65% of the 2025 market share. Their widespread adoption is attributed to regulatory requirements for continuous, real-time monitoring in urban and industrial environments. Indoor monitoring systems are gaining traction, particularly in hospitals, schools, and offices, where maintaining safe air quality is critical. Portable and wearable AQMS solutions are emerging as a growth segment, providing personal exposure data and supplementing fixed monitoring networks.

Pollutant Type Insights

Chemical pollutants such as NO₂, SO₂, CO, and O₃ dominate the monitoring landscape, forming around 55% of the global market in 2025. These pollutants are primarily emitted from vehicular, industrial, and power generation sources. Particulate matter (PM2.5 and PM10) monitoring is also increasing due to its severe health impacts, particularly in urban centers with high traffic density and industrial activity.

Sampling Method Insights

Continuous or active sampling systems lead the market due to their ability to deliver real-time, accurate data. These systems are essential for regulatory compliance, emergency alerts, and industrial process monitoring. Passive sampling methods are used primarily in research studies or supplementary monitoring networks where cost-effectiveness is prioritized over real-time data.

End-Use Insights

The government and municipal sector accounts for the largest share of AQMS demand, as regulatory compliance and public health monitoring drive widespread adoption. Industrial and manufacturing facilities are the second-largest users, deploying monitoring systems to comply with emission standards. Healthcare and educational institutions are emerging segments, emphasizing indoor air quality monitoring for improved health outcomes. Export-driven demand is increasing from developing countries importing AQMS to meet urbanization and industrialization-driven air quality challenges.

Explore more data points, trends and opportunities Download Free Sample Report

Air Quality Monitoring System Market Segmentations

By Product

- Fixed

- Portable

- Wearable

By Pollutant

- PM2.5/PM10

- VOCs

- CO2

- NO2

By End-use

- Residential

- Commercial

- Industrial

Regional Insights

North America

North America holds the largest market share (36% in 2025), driven by stringent environmental regulations, high technological adoption, and established monitoring networks in the U.S. and Canada. Smart city initiatives, industrial emissions monitoring, and government-funded programs sustain growth in the region.

Europe

Europe contributes around 28% of the 2025 market. The EU mandates and high public awareness encourage extensive deployment of AQMS. Germany, France, and the U.K. lead in sensor density and smart monitoring networks, while Italy and Spain are adopting IoT-enabled solutions to monitor urban air quality.

Asia-Pacific

APAC is the fastest-growing region due to rapid industrialization, urbanization, and rising pollution levels. China and India are investing heavily in national monitoring networks, while Japan, South Korea, and Australia are integrating smart city frameworks with AQMS. The adoption rate in APAC is expected to surpass Europe by 2027 in terms of new deployments.

Middle East & Africa

The region is expanding adoption, with the UAE, Saudi Arabia, and South Africa investing in both industrial and urban air quality monitoring. Growth is driven by increasing awareness of pollution-related health impacts and government-funded infrastructure projects.

Latin America

Brazil and Mexico are leading AQMS adoption, focusing on urban air quality improvement. Growth is moderate but supported by government programs and industrial emissions monitoring initiatives.

Key Players in the Air Quality Monitoring System Market

- Thermo Fisher Scientific

- Horiba Ltd.

- Siemens AG

- Enviro Technology Services Ltd.

- Honeywell International Inc.

- Palas GmbH

- Aeroqual Ltd.

- TSI Incorporated

- Amphenol Advanced Sensors

- Urban Air Quality Monitoring Solutions

- Met One Instruments Inc.

- F&J Specialty Products

- Teledyne Technologies

- Trolex Ltd.

- GrayWolf Sensing Solutions