Gluten-Free Facial Products Market Size

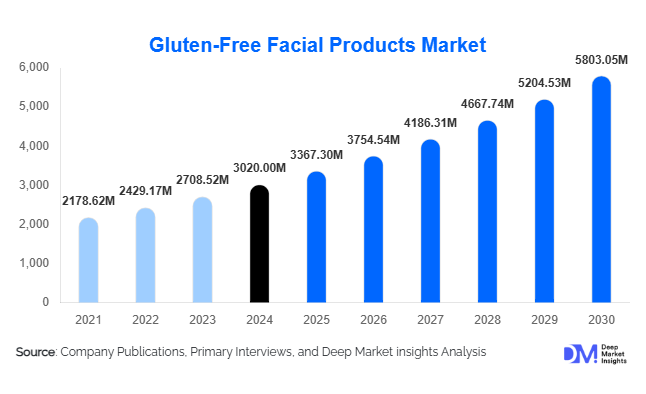

According to Deep Market Insights, the global gluten-free facial products market size was valued at USD 3,020 million in 2025 and is projected to grow from USD 3,367.30 million in 2026 to reach USD 5,803.05 million by 2031, expanding at a CAGR of 11.5% during the forecast period (2026–2031). The market growth is primarily driven by rising consumer awareness of gluten sensitivity, increasing adoption of clean and natural beauty products, and expansion of e-commerce and specialty retail channels for niche skincare offerings.

Key Market Insights

- Gluten-free facial products are increasingly integrated with clean, vegan, and organic skincare trends, catering to consumers seeking allergy-safe, ethical, and multi-functional skincare solutions.

- Moisturizers, creams, and serums dominate product demand, due to daily usage and the need for sensitive-skin formulations with gluten-free assurance.

- North America holds the largest market share, led by the U.S., due to high consumer awareness, strong clean-beauty culture, and wide availability of certified gluten-free products.

- Asia-Pacific is the fastest-growing region, driven by rising middle-class income, increasing e-commerce penetration, and growing awareness of allergen-safe skincare in China, India, and Southeast Asia.

- Technological adoption, including e-commerce platforms, direct-to-consumer digital marketing, and online skincare education, is facilitating consumer access and boosting market growth.

- Regulatory and certification initiatives, including third-party gluten-free verification, are strengthening consumer trust and driving premium product adoption.

Gluten-Free Facial Products Market latest trends

Clean and Multi-Functional Formulations

Brands are increasingly formulating gluten-free facial products with additional benefits such as anti-aging, brightening, hydration, UV protection, and barrier repair. Consumers are prioritizing products that combine multiple skincare benefits with allergy-safe ingredients. Multi-free claims such as gluten-free, fragrance-free, and vegan are becoming a standard expectation, enhancing consumer trust and appeal. Innovation in plant-based actives, botanical extracts, and sustainable ingredients is driving product differentiation and premium pricing.

Digital and E-Commerce Expansion

E-commerce channels dominate the gluten-free facial products market, providing global reach to niche and boutique brands. Consumers are using online platforms to access detailed ingredient information, reviews, and certified products, boosting confidence in gluten-free claims. Digital marketing campaigns, social media influencers, and AR/AI-based skin analysis tools are enhancing consumer engagement, education, and conversion. Online retail is also facilitating cross-border exports, helping brands penetrate emerging regions where domestic production is limited.

Gluten-Free Facial Products Market key drivers

Rising Health Awareness and Allergen Sensitivity

Increasing diagnosis of celiac disease, gluten sensitivity, and skin conditions such as eczema and dermatitis is driving consumer demand for gluten-free skincare. Consumers are actively seeking products that minimize irritation and allergic reactions, particularly for sensitive skin. Awareness campaigns and educational content via social media have further amplified the adoption of gluten-free facial products.

Growth of Clean and Natural Beauty Trends

Consumers are showing a preference for clean, organic, and ethically sourced skincare products. Gluten-free claims complement these trends, creating synergy with vegan, cruelty-free, and eco-friendly positioning. The demand for multi-functional, safe, and transparent formulations is prompting brands to invest in product development and premium formulations.

Gluten-Free Facial Products Market restraints

Labeling Ambiguity and Regulatory Gaps

The absence of stringent global regulations for gluten-free labeling in cosmetics creates uncertainty for consumers. Many products rely on self-declared claims, leading to mistrust and potential liability for brands. Variability in regulatory standards across countries complicates international expansion and certification processes.

Premium Pricing and Cost Constraints

Gluten-free formulations, particularly those with certifications or multi-free claims, carry higher production costs. Raw material sourcing, testing for gluten contamination, and smaller-scale manufacturing contribute to elevated prices. Price-sensitive consumers in emerging markets may limit adoption, especially for premium and boutique brands.

Gluten-Free Facial Products Market key opportunities

Expansion in Emerging Markets

Asia-Pacific, Latin America, and parts of the Middle East represent untapped growth regions. Increasing disposable incomes, rising awareness of skin allergies, and growth in e-commerce adoption present strong opportunities for both local and international brands. Tailoring formulations to regional skin types, climate, and consumer preferences can accelerate penetration and brand loyalty.

Innovation in Multi-Functional Products

Integrating anti-aging, brightening, and UV protection in gluten-free facial products allows brands to capture broader consumer segments. Botanical actives, probiotics, and other novel ingredients are emerging as differentiators. Brands that effectively combine efficacy, safety, and allergen-free positioning can gain premium market share and strengthen consumer trust.

Certification and Labeling Leadership

Securing third-party gluten-free certification enhances credibility and provides a competitive advantage. As regulations evolve, early adoption of certified labeling practices will allow brands to position themselves as leaders in safety, transparency, and quality. Leveraging certifications in marketing campaigns can build loyalty among sensitive-skin consumers and healthcare professionals recommending gluten-free skincare.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3020 Million |

| Market Size in 2026 | USD 3367.30 Million |

| Market Size in 2031 | USD 5803.05 Million |

| CAGR | 11.5% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Moisturizers and creams dominate the gluten-free facial products market, accounting for 30-35% of the 2025 market. These products are essential for daily skincare routines and are particularly relevant for sensitive or reactive skin. Serums and masks are growing rapidly due to rising consumer interest in multi-functional and treatment-oriented formulations. Clean and natural positioning strengthens market appeal, with premium and mid-premium tiers capturing a large share of consumer spending.

Application Insights

Daily facial skincare remains the primary application, particularly for consumers with sensitive or allergy-prone skin. Anti-aging, brightening, and barrier-repair applications are emerging as high-growth segments. Spas, wellness centers, and dermatology clinics are increasingly adopting gluten-free facial products for professional treatments. Export-driven demand from North America and Europe to emerging regions also supports growth in specialty applications, including spa and clinical use.

Distribution Channel Insights

Online platforms are the leading distribution channels, offering global reach, product transparency, and consumer education. Specialty stores and pharmacies remain critical for trust-building and professional endorsements. Direct-to-consumer models, subscription boxes, and boutique retail outlets are emerging as alternative engagement channels, particularly for premium and indie brands. E-commerce also facilitates cross-border sales, enabling smaller brands to access emerging markets with limited physical retail infrastructure.

End-User Insights

Women constitute the largest end-user group, accounting for over 60% of market demand, though men’s and unisex products are growing rapidly. Teenagers and younger adults are adopting gluten-free products due to awareness of skin sensitivities and clean beauty trends. Older adults increasingly prefer anti-aging and barrier-repair formulations. Dermatology and clinical skincare applications are emerging as high-value end-use segments, complementing consumer retail demand.

Age Group Insights

Consumers aged 31–50 represent the largest segment, driven by higher disposable income and awareness of skincare health. The 18–30 age group is fueling growth through online purchases and a preference for natural, multi-free, and influencer-endorsed brands. Older demographics, 51–65 years, increasingly adopt premium gluten-free skincare, particularly anti-aging and sensitive-skin products. Products for children and teens remain niche but growing, driven by parents seeking hypoallergenic and safe formulations.

Explore more data points, trends and opportunities Download Free Sample Report

Gluten-Free Facial Products Market Segmentations

By Product Type

- Moisturizers & Creams

- Serums

- Masks

- Eye Creams & Treatments

- Cleansers & Toners

By Application

- Daily Skincare

- Anti-Aging

- Brightening & Pigmentation

- Barrier Repair & Sensitive Skin

- Professional/Clinical Treatments

By Distribution Channel

- Online Retail (E-commerce)

- Specialty Stores & Pharmacies

- Direct-to-Consumer (D2C)

- Boutique Retail

- Spas & Dermatology Clinics

By End-User

- Women

- Men

- Teens & Young Adults

- Older Adults

Regional Insights

North America

North America dominates the market, led by the U.S. and Canada, accounting for 40-45% of global revenue in 2025. High consumer awareness, strong clean-beauty culture, certified gluten-free labeling, and e-commerce penetration drive demand. Moisturizers, serums, and daily-use creams are the most popular categories. The region also serves as a hub for exports to emerging markets.

Europe

Europe holds 25-30% of the market, led by the U.K., Germany, and France. Consumers favor organic, vegan, and certified allergen-free products. Regulatory frameworks and sustainability initiatives support premium positioning. Emerging Eastern European markets are growing faster due to increasing disposable income and rising skincare awareness.

Asia-Pacific

APAC is the fastest-growing region, driven by China, India, Japan, South Korea, and Southeast Asia. Expanding middle-class populations, increasing e-commerce adoption, and rising awareness of allergens contribute to growth. Both premium and mid-tier gluten-free products are gaining traction, particularly through online channels and urban retail.

Latin America

Latin America is growing slowly, with Brazil, Mexico, and Argentina leading. Affluent urban populations are adopting gluten-free skincare, though market penetration is constrained by price sensitivity and limited local production. Imports of premium products from North America and Europe support demand.

Middle East & Africa

MEA accounts for 3-5% of the market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. High-income consumers prefer premium and luxury gluten-free skincare. In Africa, urban centers are increasingly adopting imported skincare products with allergy-safe positioning, supporting niche growth.

Key Players in the Gluten-Free Facial Products Market

- Eminence Organic Skin Care

- Beautycounter

- Paula’s Choice

- Juice Beauty

- Alba Botanica

- Nude by Nature

- First Aid Beauty

- Derma E

- MyChelle Dermaceuticals

- Avène

- Clinique

- La Roche-Posay

- Neutrogena

- Dr. Hauschka

- Kiehl’s