Audiobooks Platforms for Kids Market Size

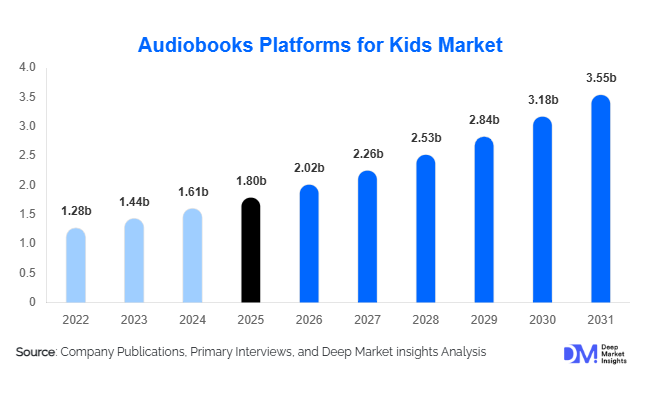

According to Deep Market Insights, the global audiobooks platforms for kids market size is estimated at USD 1.8 billion in 2025 and is projected to grow to USD 2.02 billion in 2026, reaching approximately USD 3.55 billion by 2031, representing an estimated CAGR of 12.0% during the forecast period (2026-2031). Growth is being driven by rising parental demand for screen-time alternatives, increased investment in interactive and educational audio content, and the expansion of subscription-based children’s audio services tailored to diverse learning needs and multilingual households.

Key Market Insights

- Platforms are shifting from passive listening to adaptive, interactive audio experiences, integrating assessments, branching narratives, and voice-driven interactions that support literacy and attention-span development.

- Content diversification toward multicultural and regional dialect storytelling is rising, with more titles produced in minority languages and authentic accents to support cultural identity and language preservation.

- Subscription models dominate monetization, but hybrid freemium strategies with in-app purchases for premium interactive modules are gaining traction.

- Educational partnerships with schools and tutoring platforms are emerging as a high-value channel, allowing platforms to embed curricula-aligned audio lessons for early readers.

- Neurodiversity-oriented features — adjustable narration speed, simplified sentence modes, and sensory-friendly soundscapes — are becoming key differentiators for retention.

- Voice assistant and smart speaker integration is accelerating at-home usage, turning living rooms into low-screen listening zones that parents value for bedtime and car routines.

Audiobooks Platforms for Kids Market Trends

AI-Powered Adaptive Storytelling

Platforms are deploying AI systems that adjust narration complexity, vocabulary, and pacing based on comprehension checks and engagement signals, making the audiobooks platforms for kids market more personalized and learning-focused.

Bilingual & Code-Switching Audio Titles

Publishers are introducing bilingual stories with intentional language switching and parallel narration tracks, positioning the audiobooks platforms for kids industry as a tool for second-language acquisition and multilingual education.

Audiobooks Platforms for Kids Market Drivers

Parent-Led Demand for Low-Screen Educational Content

Parents seeking screen-free alternatives are adopting audio-first learning experiences, with the audiobooks platforms for kids market gaining traction through curriculum-mapped playlists that support imagination and literacy.

Integration with Education & Licensing Opportunities

Schools and libraries are licensing large-scale audio libraries for remote learning and literacy support, making the audiobooks platforms for kids market attractive for institutional revenue streams beyond subscriptions.

Audiobooks Platforms for Kids Market Restraints

Discoverability Challenges for Niche and Regional Content

Franchise-heavy catalogs make it hard for regional and independent stories to gain visibility, limiting the diversity of offerings in the audiobooks platforms for kids market.

Perceived Value Gap Among Caregivers

Some parents see audio content only as entertainment, which reduces willingness to pay premium fees and creates churn risks in the audiobooks platforms for kids market.

Audiobooks Platforms for Kids Market Opportunities

Micro-Learning Audio Modules & Homework Integration

Short, curriculum-aligned lessons such as phonics drills and vocabulary boosters create adoption pathways into schools and after-school programs, opening new segments for the audiobooks platforms for kids market.

Smart Toy & Voice-First Product Bundles

Integrating audiobooks with smart toys and voice-enabled devices enhances multisensory engagement and expands monetization opportunities for the audiobooks platforms for kids market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.8 billion |

| Market Size in 2026 | USD 2.02 billion |

| Market Size in 2031 | USD 3.55 billion |

| CAGR | 12.0% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Content splits into interactive/adaptive audiobooks, traditional narrated story libraries, educational micro-modules (phonics, language lessons), and franchise/IP-based audio dramas. Interactive/adaptive titles command higher ARPU due to custom modules and in-app unlocks, while long-tail narrated libraries drive subscriber breadth and retention.

Application Insights

The most popular applications are bedtime stories, commute/listen-along content, early literacy curricula support, and language-learning tracks. Newer applications include therapeutic audio for emotional regulation and social skills training, and creative writing sparkers that invite children to record alternate endings.

Distribution Channel Insights

Direct-to-consumer subscription apps and in-app purchases remain primary channels. Partnerships with schools and libraries (institutional licensing), integrations with smart speaker marketplaces, and bundling with educational tablet devices are growing secondary channels. Cross-promotion via children’s publishers and podcast platforms also extends reach.

Explore more data points, trends and opportunities Download Free Sample Report

Audiobooks Platforms for Kids Market Segmentations

Product Type

- Interactive & Adaptive Audiobooks

- Traditional Narrated Storybooks

- Educational Micro-Learning Modules

- Franchise & IP-Based Audio Dramas

Application

- Bedtime & Entertainment Stories

- Early Literacy & Reading Support

- Language Learning & Bilingual Education

- Therapeutic & Emotional Development Audio

Distribution Channel

- Direct-to-Consumer Subscription Apps

- School & Library Licensing

- Smart Speaker & Voice Assistant Integration

- Partnerships with EdTech Platforms

- Regional & Localized Audio Publishing Apps

Regional Insights

North America: Largest Consumer Market

North America remains the largest consumer market for kids’ audiobooks platforms, driven by high household spending on educational technology and early adoption of subscription-based models. The U.S. leads in market share due to widespread smart device usage, robust publisher-platform partnerships, and high parental awareness of developmental benefits. Canada shows strong growth in bilingual audiobook demand, particularly English-French offerings, aligned with national education policies. The region also benefits from the integration of audiobooks into public library systems and K-12 educational curricula.

Europe: High Penetration of Multilingual Content

Europe is a mature market characterized by strong uptake of multilingual and culturally diverse audiobook libraries. Countries such as Germany, the U.K., and France dominate subscription revenues, while Northern and Eastern Europe are seeing steady growth through regional-language titles. Regulatory frameworks like GDPR significantly impact product design, pushing platforms to strengthen parental controls and data privacy features. Demand is reinforced by national initiatives supporting digital literacy in schools, and markets with high immigrant populations (Germany, Netherlands, Sweden) show accelerating demand for bilingual and multicultural story content.

Asia-Pacific: Rapid Subscriber Growth

Asia-Pacific is the fastest-growing region for kids’ audiobook platforms. Growth is fueled by rising disposable income, large school-age populations, and mobile-first consumption patterns. China and India represent the largest opportunities due to the rapid adoption of regional-language content, expanding smartphone penetration, and government-backed digital education initiatives. Japan, South Korea, and Australia show demand for premium and bilingual titles, while Southeast Asia is adopting ad-supported or low-cost subscription models. Partnerships with local publishers and edtech platforms are essential for scale in this fragmented market.

Latin America

Latin America is in the early adoption phase, with growth concentrated in Brazil, Mexico, and Argentina. Expansion is supported by increasing smartphone use, affordable data packages, and telco-led partnerships that bundle audiobook apps with mobile subscriptions. Spanish- and Portuguese-language content dominates, with rising interest in culturally relevant storytelling that aligns with regional traditions. Education-focused programs and NGO-led literacy initiatives also play a significant role in boosting access, particularly in underserved areas where print books are limited.

Middle East & Africa

The Middle East & Africa market is nascent but developing steadily. The UAE and Saudi Arabia are leading in adoption, driven by high-income households, smart device penetration, and government investment in education technology. In Africa, growth is supported by NGO and education-sector partnerships using audiobooks as cost-effective literacy tools in regions with low access to print materials. Local-language audio production is a critical enabler, with early traction seen in South Africa, Nigeria, and Kenya. Expansion in this region depends heavily on low-bandwidth streaming solutions and offline listening capabilities.

Company Market Share

The market is moderately consolidated among global audio and streaming incumbents for mass-market titles, while dedicated kids’ audiobook specialists and educational startups capture niche segments. Leading platforms account for a significant portion of paid subscriptions, while numerous smaller publishers and local apps dominate regional language niches.

Key Players in the Audiobooks Platforms for Kids Market

- Audible (incl. Audible for Kids)

- Storytel

- Spotify (Kids and family content initiatives)

- Apple Books

- Google Play Books

- Epic!

- Various regional specialists and educational startups

Recent Developments

- In 2025, at the Bologna Children's Book Fair, Audible announced a 28% year-over-year growth in its kids’ audio listening segment. The company also introduced kid-friendly profiles within its app, aimed at providing a safe and engaging listening environment for young audiences. This update was highlighted during industry discussions on balancing creativity with market expansion in the children’s audiobooks space.