Brand Licensing Market Size

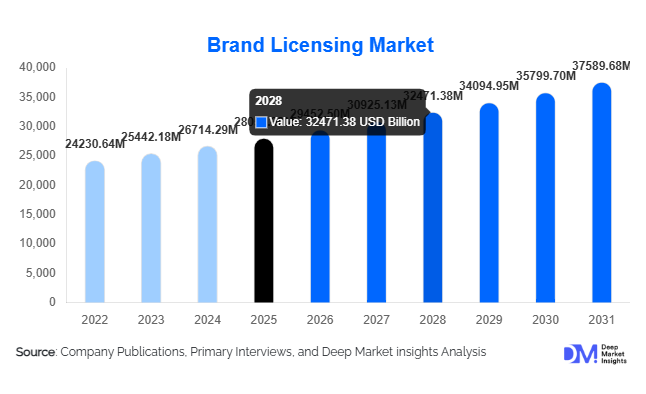

According to Deep Market Insights, the global brand licensing market size was valued at USD 28,050.00 million in 2025 and is projected to grow from USD 29,452.50 million in 2026 to reach USD 37,589.68 million by 2031, expanding at a CAGR of 5.0% during the forecast period (2026–2031). The growth of the brand licensing market is primarily driven by a surge in digital licensing, an expanding consumer appetite for branded merchandise, and the diversification of licensing into non-traditional product categories, such as digital goods, sustainability-linked merchandise, and corporate co-branding partnerships.

Key Market Insights

- Apparel licensing dominates the global landscape, accounting for approximately 28% of total brand licensing revenue in 2025, driven by fashion collaborations and character-based merchandise.

- Entertainment licensing remains the largest application segment, capturing nearly 40% of the market due to film, gaming, and media IP extensions across global platforms.

- North America leads the global market with roughly a 55% share in 2025, supported by strong entertainment IP portfolios and mature retail networks.

- Asia-Pacific is the fastest-growing regional market, with China and India emerging as major contributors due to rising disposable incomes and expanding e-commerce adoption.

- Digital and virtual licensing opportunities, including gaming skins, avatars, and NFT merchandise, are redefining the licensing ecosystem and driving incremental revenue streams.

- Corporate and sustainability-focused licensing models are emerging as key growth frontiers, enabling brands to extend into eco-friendly product categories and purpose-driven collaborations.

Latest Market Trends

Digital and Virtual Licensing Transforming IP Monetization

The rapid rise of digital ecosystems, encompassing video games, metaverse environments, and virtual collectibles, is reshaping how brand owners monetize intellectual property. Licensors now extend their characters, logos, and trademarks into virtual spaces, creating digital avatars, NFT drops, and in-game branded assets. This trend reduces production overheads and accelerates global reach, enabling fans to engage with their favorite brands in immersive ways. As gaming and social platforms evolve, digital licensing is expected to become a multi-billion-dollar revenue stream within the broader brand licensing industry.

Collaborative Fashion and Lifestyle Licensing

Fashion collaborations remain a core pillar of the licensing market, with designer labels and entertainment franchises partnering for capsule collections and limited-edition apparel lines. Co-branding between luxury houses and pop culture icons has created strong demand among Gen Z and Millennial consumers. Lifestyle licensing is also expanding into home décor, accessories, and wellness products, aligning with consumers’ aspirations for brand-driven identity and sustainability-conscious consumption. These collaborations often feature limited runs, premium pricing, and online-exclusive launches to heighten consumer engagement.

Brand Licensing Market Drivers

Expanding Consumer Demand for Branded Goods

Global consumers increasingly associate branded merchandise with identity, status, and authenticity. Entertainment-driven merchandise, sports apparel, and fashion collaborations are key contributors. Millennials and Gen Z shoppers favor character-based and influencer-endorsed products, driving sustained market growth.

Growth of E-commerce and Digital Retail Channels

E-commerce now represents nearly 37% of global licensing sales, transforming how consumers access branded goods. Online platforms enable faster distribution, data-driven personalization, and cross-border reach, allowing licensors and licensees to expand without traditional retail overheads.

Diversification into New Product Categories

Licensing has expanded beyond apparel and toys into food, beverages, home furnishings, and digital products. Cross-sector partnerships, such as branded snacks, household items, or limited-edition furniture, create new monetization channels and deepen brand loyalty.

Market Restraints

IP Management and Counterfeiting Challenges

Complex multi-country licensing agreements require rigorous IP oversight. Counterfeiting and unauthorized usage threaten brand equity and erode royalty revenue. Managing global contracts and enforcing compliance remains a significant operational challenge for licensors.

Market Saturation and Over-Licensing Risk

As more brands pursue licensing, oversaturation in certain product categories can lead to diminished consumer exclusivity and weakened brand perception. Balancing the quantity of deals with quality and authenticity has become critical for maintaining long-term profitability.

Brand Licensing Market Opportunities

Digital & Virtual Licensing Expansion

Digital ecosystems present an unprecedented growth channel for licensing. Brands can extend IP into metaverse environments, video games, and social commerce. Virtual goods, character skins, and branded digital collectibles are driving new monetization models and fan engagement strategies.

Emerging Market Penetration

Asia-Pacific and Latin America represent the next growth frontiers for brand licensing. Rising middle-class incomes, improved IP laws, and booming e-commerce infrastructure in China, India, and Brazil are opening doors for localized licensing partnerships. These regions are expected to record CAGRs exceeding 8% through 2031.

Corporate Sustainability & Co-Branding

Corporate licensing that integrates sustainability principles, such as eco-friendly materials, ethical production, and community-driven initiatives, offers brands reputational and financial benefits. ESG-compliant licensing programs attract conscious consumers and align with regulatory trends worldwide.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28050 Million |

| Market Size in 2026 | USD 29452.50 Million |

| Market Size in 2031 | USD 37589.68 Million |

| CAGR | 5.0% (2026- 2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026- 2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Apparel Licensing dominates the global brand licensing market, holding about 28% market share in 2025 (valued at approximately USD 87 billion). Apparel remains the most visible and high-volume category due to its consistent consumer turnover, deep fashion collaborations, and strong entertainment tie-ins across franchises and character-based designs. Other major segments include Toys & Games (18%), Accessories (12%), and Home Décor (10%). The fastest-growing category is Software & Video Game Licensing, expanding at a rate above 8% CAGR, driven by digital transformation, gaming IP monetization, and the rise of virtual merchandise and NFTs.

Application Insights

Entertainment Licensing continues to anchor the industry, accounting for approximately 40% of global revenues (around USD 124 billion in 2025). This dominance is attributed to the enduring success of blockbuster film franchises, franchise-driven merchandise ecosystems, and cross-media branding strategies that extend across streaming, gaming, and live events. Fashion and Sports Licensing collectively capture nearly 30% of the global total, boosted by celebrity collaborations, luxury extensions, and growing fan engagement in sports merchandise.

Distribution & End-Use Insights

Retail & E-commerce represent the largest distribution and end-use segment, commanding more than one-third of total global licensing revenues (USD 115 billion in 2025). Online marketplaces, omnichannel retailing, and the rise of direct-to-consumer (D2C) licensing models have revolutionized how brands reach consumers globally. Sports, entertainment, and fashion companies are leveraging hybrid physical-digital sales networks, while consumer goods and FMCG manufacturers increasingly use licensing for market differentiation and regional expansion.

Explore more data points, trends and opportunities Download Free Sample Report

Brand Licensing Market Segmentations

By Product Category

- Apparel & Footwear

- Toys & Games

- Home Décor & Housewares

- Food & Beverage

- Consumer Electronics

- Health & Beauty Products

- Publishing & Media Content

- Stationery & Gifts

- Sports Merchandise

- Luxury Goods & Accessories

By Licensing Type

- Corporate Brand Licensing

- Entertainment & Character Licensing

- Sports Licensing

- Fashion Licensing

- Art & Design Licensing

- Collegiate & Non-Profit Licensing

- Celebrity & Influencer Licensing

- Music Licensing

By Distribution Channel

- Online Retail (E-commerce Platforms)

- Department & Specialty Stores

- Mass Retailers & Hypermarkets

- Direct-to-Consumer (D2C) Brand Stores

- Franchise Outlets

- Entertainment & Theme Parks

By End Use Industry

- Entertainment & Media

- Fashion & Lifestyle

- Sports & Recreation

- Retail & E-commerce

- Food & Beverage

- Publishing & Education

- Technology & Gaming

- Hospitality & Events

Regional Insights

North America

North America dominates the brand licensing market, generating approximately 55% of global revenue (USD 170 billion in 2025). The United States leads with a robust ecosystem of entertainment, sports, and fashion licensing. Deep consumer brand affinity, extensive retail infrastructure, and mature intellectual property protection frameworks sustain consistent regional growth.

Europe

Europe contributes around 25–30% of the global market share (USD 80–90 billion). Major markets include the U.K., Germany, France, and Italy, supported by luxury fashion houses, automotive brand extensions, and strong sports licensing portfolios. Rising sustainability consciousness and ethical production standards are reshaping brand partnerships and licensing strategies across the continent.

Asia-Pacific

The Asia-Pacific region accounts for roughly 15–20% of the market (USD 45–60 billion) and is the fastest-growing region. Key drivers include booming domestic IP creation in China, Japan, and India, increasing cross-border licensing deals, and expanding digital and e-commerce ecosystems. Localized entertainment IP and fashion collaborations are accelerating consumer engagement and regional brand monetization.

Latin America

Latin America represents about 4–6% of the global market (USD 15 billion), led by Brazil, Mexico, and Argentina. Growth is driven by rising middle-class consumption, formalization of retail channels, and the growing appeal of licensed sports and lifestyle merchandise.

Middle East & Africa

Middle East & Africa (MEA) contributes approximately 2–4% of total market value (USD 6–12 billion). The GCC nations dominate demand, driven by affluent consumers, mall-based retail ecosystems, and an expanding appetite for luxury brand licensing. Meanwhile, select African markets are emerging as new growth frontiers in entertainment and sports merchandising, supported by improving retail infrastructure and youth-led consumer trends.

Key Players in the Brand Licensing Market

- The Walt Disney Company

- Hasbro Inc.

- Mattel Inc.

- Authentic Brands Group

- PVH Corp.

- Sanrio Co., Ltd.

- Universal Brand Development

- Nickelodeon (Paramount Global)

- National Football League (NFL)

- Major League Baseball (MLB)

- WWE Inc.

- Ferrari N.V.

- General Motors Company

- Electrolux AB

- Learfield IMG College