Toy Market Size

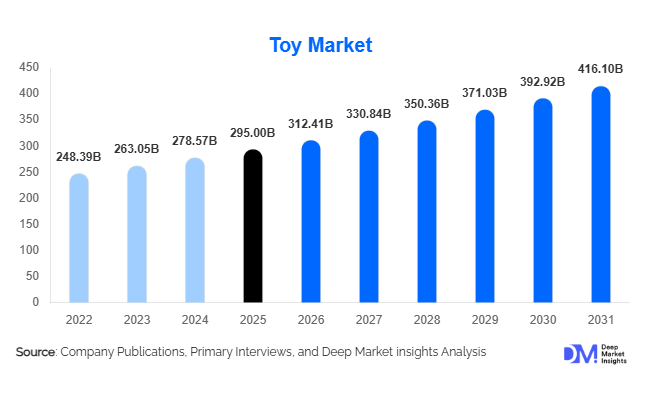

According to Deep Market Insights, the global toy market size was valued at USD 295.0 billion in 2025 and is projected to grow from USD 312.41 billion in 2026 to reach USD 416.10 billion by 2031, expanding at a CAGR of 5.9% during the forecast period (2026–2031). The toy market growth is primarily driven by rising disposable income, increasing demand for educational and STEM-based toys, and the growing influence of entertainment franchises and digital gaming ecosystems on children’s products. The industry has evolved significantly from traditional playthings to interactive, technology-enabled products that combine learning with entertainment.

In recent years, toy manufacturers have focused heavily on innovation, integrating artificial intelligence, augmented reality, and connected applications into toy experiences. Educational toys, robotics kits, and coding toys are witnessing particularly strong demand as parents increasingly prioritize developmental benefits alongside entertainment value. Another major growth driver is the emergence of the “kidult” demographic, adult consumers who purchase collectibles, building sets, and nostalgic toys for leisure and hobby activities.

Retail dynamics have also shifted dramatically as e-commerce channels continue to gain market share. Online marketplaces, brand-owned digital stores, and social media-driven marketing campaigns are transforming the way toys are discovered and purchased globally. Meanwhile, licensing partnerships with major film studios, gaming companies, and entertainment brands continue to drive seasonal demand and product launches.

Regionally, North America and Europe represent mature markets with high per-capita spending on toys, while Asia-Pacific is emerging as the fastest-growing region due to demographic expansion, rising middle-class incomes, and expanding retail infrastructure. Overall, the toy market is transitioning toward integrated learning, digital engagement, and cross-media entertainment ecosystems, positioning it for sustained growth through the end of the decade.

Key Market Insights

- Educational and STEM toys are becoming a central growth driver, as parents increasingly prioritize products that support cognitive development and learning.

- The “kidult” consumer segment is expanding rapidly, with adults purchasing collectibles, construction sets, and nostalgic toys for hobby and stress-relief purposes.

- North America dominates the global toy market, supported by strong retail infrastructure, high consumer spending, and strong licensing partnerships.

- Asia-Pacific is the fastest-growing regional market, fueled by demographic growth, rising disposable incomes, and expanding e-commerce penetration.

- E-commerce platforms are reshaping toy distribution, offering consumers broader product selection, transparent pricing, and direct access to brands.

- Technology-enabled toys, including AI-powered robots and app-connected play systems, are transforming the traditional toy industry.

What are the latest trends in the toy market?

Rise of STEM and Educational Toys

Educational toys focusing on science, technology, engineering, and mathematics are rapidly gaining popularity worldwide. Parents and educators increasingly prefer toys that encourage problem-solving, creativity, and analytical thinking. Robotics kits, engineering construction sets, and coding toys are becoming common in both homes and classrooms. This trend is particularly strong in North America, Europe, and parts of Asia where educational systems emphasize early STEM learning. Toy manufacturers are partnering with schools and educational technology companies to integrate learning tools into play environments. As a result, STEM toys are transitioning from niche products to mainstream educational tools that support childhood development.

Integration of Smart and Connected Toys

Technological innovation is transforming the toy market as manufacturers introduce connected toys that interact with mobile applications and cloud-based systems. Smart toys equipped with artificial intelligence can respond to voice commands, personalize gameplay, and adapt learning activities based on user behavior. Augmented reality games are also merging physical play with digital experiences, enabling children to interact with toys through smartphones or tablets. These innovations are attracting digitally native consumers who seek immersive and interactive entertainment. Companies are increasingly investing in digital ecosystems that combine toys with gaming platforms, educational apps, and subscription-based content services.

What are the key drivers in the toy market?

Growing Disposable Income and Consumer Spending

Rising household incomes across both developed and emerging economies have increased consumer spending on children’s entertainment and educational products. Parents are willing to invest in higher-quality toys that provide developmental benefits or extended play value. In rapidly developing markets such as China, India, and Southeast Asia, expanding middle-class populations are significantly boosting toy consumption. Increased purchasing power has also encouraged demand for premium toys, branded collectibles, and licensed products linked to popular entertainment franchises.

Influence of Entertainment Franchises and Licensing

The toy industry is closely tied to the global entertainment sector, with major toy manufacturers partnering with film studios, streaming platforms, and video game developers. Character-based toys linked to blockbuster movies, animated series, and gaming franchises often generate significant seasonal demand. Licensing agreements allow toy companies to capitalize on brand recognition and fan loyalty, driving strong sales around film releases or entertainment launches. As streaming platforms continue to expand original content, opportunities for licensed toys are also increasing.

What are the restraints for the global market?

Strict Safety Regulations and Compliance Costs

Toy manufacturers must comply with stringent safety standards across different regions to ensure child safety. Regulations covering chemical content, choking hazards, and product durability can significantly increase production and testing costs. Compliance requirements vary across countries, making it challenging for companies to scale globally without adapting products to meet regional safety standards. These regulatory complexities can slow product launches and increase operational expenses for manufacturers.

Competition from Digital Entertainment

The increasing popularity of mobile games, video game consoles, and streaming content has created strong competition for traditional toys. Children are spending more time on digital entertainment platforms, which can reduce engagement with physical toys. To remain relevant, toy manufacturers must innovate continuously by integrating digital elements into their products. Companies that fail to adapt to changing entertainment habits may struggle to maintain market share.

What are the key opportunities in the toy industry?

Expansion in Emerging Consumer Markets

Emerging economies represent one of the largest opportunities for the toy industry. Rapid urbanization, growing middle-class populations, and rising disposable incomes are expanding demand for children's products in countries such as India, Brazil, Indonesia, and Vietnam. These markets are experiencing strong growth in organized retail and e-commerce, making toys more accessible to a broader consumer base. Early investment in these regions can help companies establish strong brand recognition and long-term market share.

Innovation in Smart and Interactive Toys

The integration of advanced technologies such as artificial intelligence, augmented reality, and voice recognition is creating new categories of toys. Interactive robots, AI-powered learning companions, and AR-based games are attracting tech-savvy consumers and expanding the traditional definition of toys. Technology companies are increasingly collaborating with toy manufacturers to develop hybrid digital-physical products. This trend is expected to generate significant revenue opportunities as connected toys become mainstream.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 295.0 Billion |

| Market Size in 2026 | USD 312.41 Billion |

| Market Size in 2031 | USD 416.10 Billion |

| CAGR | 5.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Product Type Insights

Building and construction toys represent one of the most dominant product categories in the global toy market, accounting for approximately 22% of total market revenue in 2025. These toys are highly popular because they combine entertainment with educational value, encouraging creativity, spatial awareness, and problem-solving skills. Construction sets appeal to a wide range of age groups, from young children to adult hobbyists and collectors. Meanwhile, electronic and interactive toys are emerging as the fastest-growing category as manufacturers incorporate smart technologies and app connectivity. Dolls and plush toys remain a stable segment driven by character licensing and entertainment franchises, while board games and puzzles are experiencing renewed popularity among families seeking offline recreational activities.

Application Insights

The primary application of toys remains household consumption, particularly among children aged 6–12 years, which represents the largest consumer segment globally with approximately 35% share of toy demand. However, several additional applications are emerging across educational institutions, therapy programs, and hobbyist communities. Educational toys are increasingly used in classrooms to teach STEM concepts through play-based learning methods. Robotics kits and coding toys are particularly popular in schools and extracurricular programs focused on technology education. Another emerging application is the adult collector market, where consumers purchase toys for display, collecting, and hobby purposes. This “kidult” segment is expanding rapidly and contributing to premium toy sales worldwide.

Distribution Channel Insights

E-commerce platforms have become one of the most influential distribution channels in the toy industry, accounting for approximately 28% of global toy sales. Online marketplaces allow consumers to compare products easily, access a wider selection of toys, and benefit from competitive pricing. Hypermarkets and supermarkets continue to play a major role in toy retail due to high foot traffic and strong brand visibility. Specialty toy stores remain important for premium products and collectibles, offering curated selections and expert recommendations. Direct-to-consumer brand websites are also growing rapidly as manufacturers invest in digital marketing and build stronger relationships with customers through loyalty programs and exclusive online product launches.

Traveler Type Insights

While toys are primarily designed for children, consumer demographics are expanding significantly. Children aged 6–12 years represent the largest consumer group due to their engagement with diverse toy categories, including action figures, construction sets, and electronic toys. Teenagers are increasingly purchasing interactive toys and gaming-related merchandise, particularly products tied to popular video games or online content creators. Adults, commonly referred to as “kidults”, are emerging as an important consumer segment, purchasing collectible figurines, model kits, and premium building sets for hobby and leisure activities. Family purchases also play a significant role, particularly during holiday seasons when toys are bought as gifts for children and shared play experiences.

Age Group Insights

School-age children between 6 and 12 years represent the largest share of toy consumption globally due to their diverse interests and active engagement with play activities. Preschool children aged 3–5 years form another important segment, driving demand for educational toys and sensory development products. Infants and toddlers require specialized toys focused on safety, motor skill development, and sensory stimulation. Teenagers represent a smaller but growing segment, particularly for technology-enabled toys and collectible merchandise. Adults aged 18 years and above are contributing significantly to premium toy sales through collector markets and hobby-oriented purchases, particularly in developed economies.

Explore more data points, trends and opportunities Download Free Sample Report

Toy Market Segmentations

By Product Type

- Action Figures & Character Toys

- Dolls & Plush Toys

- Building & Construction Toys

- Games & Puzzles

- Educational & STEM Toys

- Electronic & Interactive Toys

- Outdoor & Sports Toys

- Infant & Toddler Toys

- Collectible & Designer Toys

By Age Group

- Infant & Toddler

- Preschool

- School-Age Children

- Teenagers

- Adults / Kidult Collectors

By Material Type

- Plastic Toys

- Wooden Toys

- Metal Toys

- Fabric & Plush Materials

- Eco-Friendly / Recycled Materials

By Distribution Channel

- Hypermarkets & Supermarkets

- Specialty Toy Stores

- Department Stores

- E-commerce Platforms

- Direct-to-Consumer

Regional Insights

North America

North America accounts for approximately 32% of the global toy market in 2025, making it the largest regional market. The United States dominates regional demand, representing nearly three-quarters of total North American toy sales. Strong consumer spending, a well-developed retail network, and extensive licensing partnerships with entertainment companies support market growth. Canada also contributes a steady demand through expanding e-commerce toy sales and rising interest in educational toys.

Europe

Europe represents roughly 26% of the global toy market. Countries such as Germany, the United Kingdom, and France are major contributors due to high household spending on children's products. European consumers increasingly prefer sustainable toys made from eco-friendly materials, prompting manufacturers to adopt greener production methods. Educational toys and board games are particularly popular across the region.

Asia-Pacific

Asia-Pacific accounts for approximately 28% of global toy demand and is the fastest-growing region in the market. China remains both the largest toy manufacturing hub and a rapidly expanding consumer market. India is emerging as one of the fastest-growing toy markets globally due to rising incomes, government initiatives promoting domestic manufacturing, and a large child population. Japan and South Korea represent mature markets with strong demand for technologically advanced toys.

Latin America

Latin America holds about 8% of global toy demand. Brazil and Mexico are the largest markets in the region, supported by growing retail infrastructure and rising middle-class spending on children’s products. Online marketplaces are increasingly influencing toy purchasing behavior in these countries.

Middle East & Africa

The Middle East and Africa region accounts for approximately 6% of global toy demand. The United Arab Emirates and Saudi Arabia represent the most significant markets due to high household incomes and strong retail sectors. In Africa, South Africa leads toy consumption as retail chains and e-commerce platforms expand.

Key Players in the Toy Market

- LEGO Group

- Mattel

- Hasbro

- Bandai Namco Holdings

- Spin Master

- MGA Entertainment

- Tomy Company

- Jakks Pacific

- Playmobil

- Ravensburger

- VTech Holdings

- Melissa & Doug

- Hornby

- Playmates Toys

- Funskool India